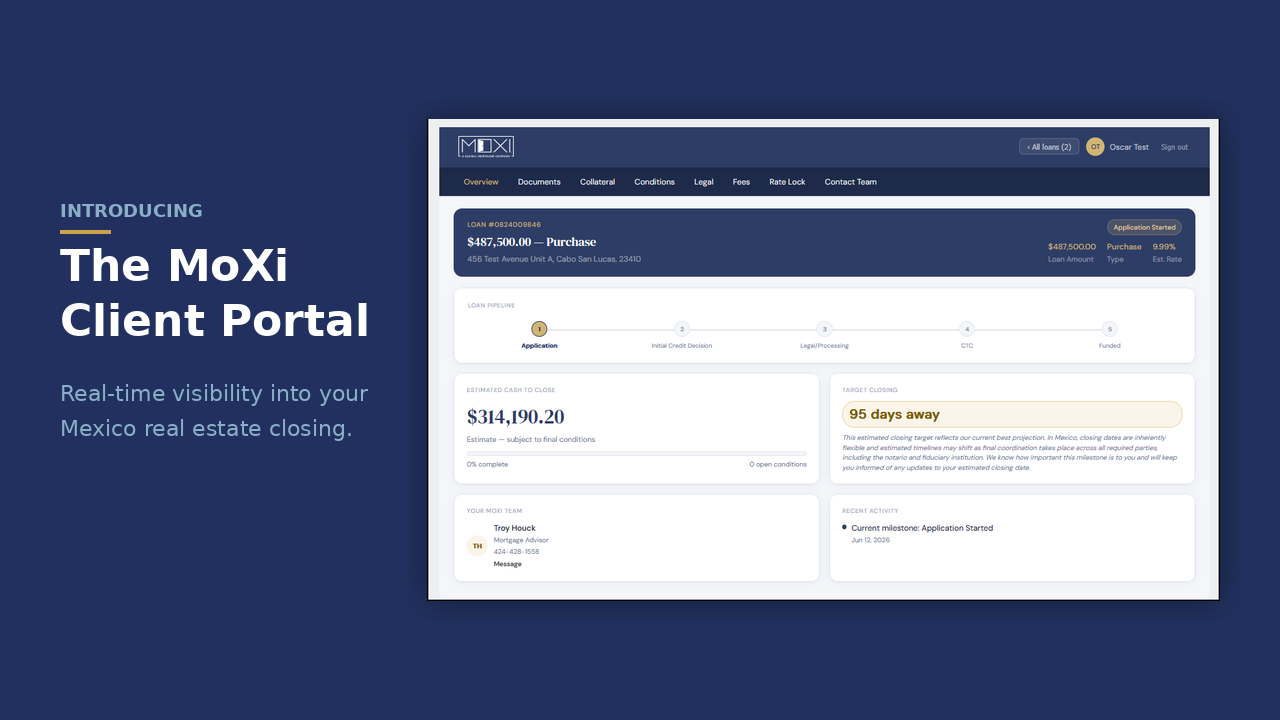

How Long Does It Take To Get A Mortgage In Mexico?

[TRANSCRIPTION]

Hi, I'm Alex Koper, CEO of MoXi. Really excited to be here today with Chris Childress, our head of retail sales, and we're going to talk today about a very exciting topic and that is mortgages in Mexico. So Chris, thanks so much for being here today.

Absolutely.

How long does the process take? How long does it take to get a mortgage in Mexico? What do you think about that?

That's a million-dollar question. So the best answer I've got for that, Alex, is going to be the speed at which we can get this thing across the finish line for everyone is directly associated with the engagement of all parties. So that starts from the very beginning, from the time that we're on a discovery call with the borrower all the way through the process. So the time at which we can get the credit approval done is directly associated with how quickly we can get a complete application from the borrower with all the information we need as well as supporting documentation that we request so that we can get in front of an underwriter and get a quality and thorough credit decision issued. Assuming everything comes in...

For example, if I have a application interview or discovery session with a borrower today, they fill out the application this evening and, say, they get me all the documents over, everything we request over today or tomorrow, it generally takes our front end team about a day or so to kind of work through the documents, get everything structured, and turned in and then moved over to the credit department. But we can arrive at a full credit decision within just a few days, generally less than a week, and that's from the date that we have the application come in and receive the documents to an actual credit decision issued and we're able to schedule a follow up call from that. So the engagement is crucial. And then the transfer part is directly associated with the engagement of all parties being really more on the seller side and the organization of the seller side and those guys. So assuming that the seller's got all their property documents in order and readily available, they're able to get it back to us quickly, respond if there's questions and all that kind of stuff, that's directly related.

Generally speaking, we see these things take 60 to 90 days. Our internal target is 45 to 60 days for a closing. To be quite candid, I've seen some disorganized sellers and issues where we've had some things with title where we've had transactions take over a year, and that's really been just working through the process of either gathering that information if they weren't quite organized or in some cases we found instances where the seller had situations like we were talking about a few minutes ago, where something wasn't recorded properly in a previous transaction and we got to work our way through cleaning those things up. So to answer your question, Alex, we generally target 60 to 90 days. Most often we see around the 90, 120 day mark to really get through working with all parties and that kind of stuff. Again, being well organized on the front end and being engaged in the process will certainly speed that along.

Those are all really good points. Yeah, it's interesting because there are controllables as it relates to MoXi certainly, but also the buyer and getting their diligence documentation and tax returns, bank statements, so on. And then there are controllables as it relates to the legal property transfer. When we send the KYC information, you have to fill it out and send it back. You'd have to send your passport copy and so on. But then there are some uncontrollers, some things totally outside of the control of the buyer. So sometimes that's seller related, sometimes it's property related. If a property's currently in a Fideicomiso, the fiduciary bank that currently holds a Fideicomiso, will they release it for substitution? Or how quickly can they process the cancellation? If the property's currently owned by a Mexican entity, how long till you get the Secretary of Foreign Affairs' permit?

So all sorts of different variables and factors. Most candidly, borrowers really can rely on MoXi to represent them through this status, but to the extent that they can be active and engaged and push their agent and/or the seller's agent and/or the seller to also be active and engaged and turn things back when they're requested, I think, that makes all the difference. I think a record closing was in a non-restricted zone was 23 days. It's the fastest we've ever done it, but it's kind of funny to think the actual loan itself takes less than a week to make, right? All those extra days are related to the legal property transfer from seller to buyer and preparing that, to do it in a secure way, which ultimately protects our customer, right?

Absolutely. Yeah, one key point is with MoXi, you've got a couple of hundred years of combined experience. Alex, you've been a couple of decades or more in C-level leadership in the mortgage industry for a long time, I've been close to 30 years now in the mortgage arena. Everyone on our team has got tons of experience in the US credit market, so we've got a lot of experience also in the Mexican legal area of that. But when it comes to underwriting and credit qualifying US borrowers, we've got that down, we've got the experience, and we can do that very efficiently in-house. Where we see the delays and the things that tend to take more time is 99% in the legal transfer portion of the process. And I can tell you that MoXi and our investors, we are as interested, if not more so, in making sure that it's done properly and legally for the sake of the security of our borrower as well as for us as a lender.

A related question to that, we will often have prospective clients come to us who are entering into a new construction contract for a property that's going to be ready in 2025, and we're recording this video in the middle of 2023. What would you recommend to someone watching this video who is buying new construction property, it won't be ready for a couple of years? Should they go through the process with this now? Should they kind of wait until they get a little closer to closing?

That's a loaded question, right? Because you don't want to start too early because there's really nothing that our team can do from a legally transfer "work" perspective until we're about 90 days out, until the development's just about ready for the delivery. That's the keys and walls up. That last 90 days generally is the dotting the I's, crossing the T's, and then making sure the legal documents are ready for legal transfer. So that's really when we're able to get involved from a legal getting-work-done type perspective. However, if the borrower is in a position where they're going to buy this property and they need financing in order to achieve this, I think it only makes sense to at least have the conversation, to at least have the discovery session. It's 30 minutes to have a conversation, get an idea of what we're working with, learn about the requirements and guidelines, and the borrow can decide at that point in time if it makes sense to go through the official pre-approval process, which involves the documents and some fees and things along those lines to get an approval in place, which we can certainly do.

But then also that borrower needs to understand that they're going to have to maintain that credit picture in order to deliver on the funding 18 months out. Does this make sense? So my thought would be is if you're a hundred percent confident, "I'm bulletproof, don't have to worry about it," here's the guidelines, let's talk 120 days out, let's get things started. Most of our borrowers, when they enter into an agreement like this and they're going to be funding the full construction of a project, expecting to be reimbursed in just a couple of years, then they might have more confidence in having the answers that they need before pulling the trigger on that. We're here to help in whatever way works best for the borrower.

Yeah, I think those are great points, and it really just depends on the comfort level of the client. And I know you spoke extensively a couple minutes back about new construction and about the fact that MoXi really can't fund a loan until legal transfer takes place, which could be at the time property delivery, but hopefully the legal transfer of the property happens at delivery at the same time. That would be probably-

Ideally.

The ideal scenario, but not always the case, right?

Yeah.

Good points. But generally at least 90 to 120 days before anticipated delivery and transfer date would be the time to apply and reach out to us. You brought up another really good point, maintaining the credit qualification throughout the escrow period. So setting aside, for just a moment, the actual new construction purchase and just thinking about a regular resale purchase, let's say you have a client that is entering into a contract, it's a 70-day escrow period, and they applied for their MoXi loan today and going to close in two months, what are some suggestions you have as it relates to maintaining credit qualification throughout that 60-70 day process to ensure no surprises at the end?

You'd be surprised at how little this question's considered. A lot of people will apply for a mortgage, they're like, "Hey, I got the approval," and go crazy. Or go start buying furniture and financing furniture for the home that they're not going to move into for six months, whatever the case is. So first and foremost, the loan approval process, we're going to look at the entire scenario for the borrower, issue a credit decision based on that. But what borrowers need to really be clear on is that they have to meet these requirements at the time of closing and funding. It's not just to get approved. So we got to make sure that whenever... Our agreement with our end investor, in order for us to close this thing and have it a fully finished deal, it has to meet our credit policy guidelines at the time of closing.

And in the US, 30-45 day churn, generally speaking. You have got to really make an effort to mess it up in that short period of time. But here with a longer lifecycle, life happens. You use your credit card to pay bills, you have a car need, or whatever the case may be. So a lot of people just don't think of the impact of those things. Just a couple of inquiries to get a new car loan could wreck a credit score and put you into a whole different qualification bucket or interest rate bucket even. So to answer your question, the key thing is that when you apply and you're issued a conditional loan approval from MoXi, one of the first things we're going to do is host what we call an ICD call with you. We have a lot of acronyms in our business. That just means initial credit decision. And we're going to jump on the phone and we're going to discuss the conditions, the terms of the approval, "Hey, we've approved this loan based off your current 750 credit score, your current debt to income ratio of this," so forth and so on.

We basically have to have the same criteria in order to fund at the same terms of that loan approval. If something changes, we have to adjust the approval for that. So if we have a credit score reduction, that means interest rate could go up or loan to value could go down. The key thing is when you make your application, when you get your loan approval, we've got a clear picture of exactly where you are and how your loan is approved at that time. It's your responsibility as the borrower to make sure that we maintain that same credit picture moving forward. And if you have any questions, anything crazy that happens during the process, call your mortgage advisor before making a move. That way we can navigate the waters together.

Those are great points. So summing it up, don't go buy a really expensive car and finance or lease it during the time of your escrow period.

That's right.

Don't purchase a bunch of furniture, maybe large purchases really that are going to appear on your credit report. Escrows get delayed, we might need to re-pull credit. We're definitely going to do a refresh at the end that won't affect the score, but we're going to know about all those things. So don't stop paying a bill, try not to have a collection appear on your credit report, try not to go apply for new credit. Those are all really good reminders. The other is about income and employment. And these are all based on situations that we've actually seen live. So I'm not just making it up, but don't change the way that you're paid. You all of a sudden decide that you're going to switch from W-2 employee to independent contractor and start operating your own business in the middle of the 60-day escrow, that's going to potentially impact your approval on your ability to even get the loan in the first place. So I think those are other really important-

Did you know that MoXi funds & services loans in USD, is regulated and audited in the US & Mexico, and ensures compliance throughout the term of your loan?

Try our MoXi Mortgage Estimator