Cabo Real Estate & Mortgage Insights (Interview)

Video Transcript - (with Alex Koper & Kenda Ruck)

Kenda:

Thank you guys so much for joining us today. I'm Kenda. I am a founding partner of a real estate brokerage in Los Cabos, Mexico called Finn Real Estate Group. And I am so thrilled to be able to be talking with you today about a real need that occurred in the real estate market in Cabo and that was for a lender to step into the forefront and help with the purchase problem that we had here in Cabo, which is the fact that lending was not really an option.

But before I introduce Alex, I would like for you guys to introduce yourselves. We want to know where you're joining us from, so please say hello and let us know where you are coming from and where you're watching from today. We want the call to be really interactive. We have also taken questions ahead of time and we would love to hear your questions as well, so we're going to do our best to answer every question that we have. We are excited to be able to chat with you and help you weed through this very complicated system that we have here. Hi, Jessica. How are you? Yay. You have a place in San Jose. I know you. Hi. Hi, Chris. How are you? Thank you so much for jumping on. We appreciate it.

Well, just a little bit of background about real estate in Cabo. About 20 years ago, a bunch of people all over the United States started realizing that Cabo is a beautiful place to live. And people in the United States started discovering Mexico and realizing that, like me, they love the culture, they love the people, they love the climate, and they, like me, really wanted to maybe start a life here or purchase property here. And like me, they had their bubble burst when they realized that buying property through any lending or getting a mortgage in Mexico is very, very difficult, if not impossible. So there was a giant hole where there needed to be some lending options and we just didn't have them for a while and historically, Mexico has just been a cash market.

Well, about five or six years ago, a company called MoXi Mortgage came on the scene and began leading the way by jumping through all of regulatory hoops and doing all of the things that they needed to do to agree with or to adapt to the anti-money laundering laws and that type of thing. So that was MoXi. And that's why I am so excited today to be able to talk to Alex Koper. Alex is the president and CEO of MoXi. MoXi is a cross-border lending company and I have a very good relationship with them. So Alex, tell us a little bit about your background and then will you tell us a little bit about some of the things that MoXi had to do to jump through the regulatory hoops to be able to offer financing in Mexico?

Alex:

Yeah. Hey, Kenda. Thanks so much for setting this up, and I think this is going to be so much fun. By the way, this is the first time we've ever done a live webinar where we actually can get questions and just in reviewing some of the questions that came in, I'm just really excited for this conversation. So again, thanks so much for having me. My name's Alex Koper. I have the pleasure of getting to work with the fantastic MoXi team. We lend across Mexico to US citizens and US permanent residents, and we have the fortunate privilege of seeing people's dreams be able to come true because of our product and program. And so it's just really, really, really lovely to be here today.

So a little bit about me. I joined up with the MoXi team about four years ago in the infancy stages of the firm. And when we talk about that ... And I know you're familiar with this, Kenda, because you are a client as well as a very successful real estate professional in the area. We have been through a lot in setting up the program. And it was really important to us at the onset that we were able to offer to clients, both from a purchase money mortgage perspective as well as from a refinancing cash or refinance perspective, a loan option that didn't really feel foreign despite the fact that it was secured by collateral in a foreign country. And so we put a lot into the way that we set up the firm. And just a couple of examples. A lot of strategic thought around what kind of entity structure to have. MoXi is comprised of really six different entities that are highly regulated and audited in Mexico and it's important.

Clients told us, prospective clients told us, "Gosh, I really want to not have any foreign exchange currency risk when I'm borrowing, so I want my loan to be in US dollars, for example. And I wanted to have a fixed interest rate and I don't really like prepayment penalties and I don't like balloon payments and I want to be able to potentially deduct my mortgage interest on my US income tax returns even though it's for my second home in Mexico." And all of these various different factors that came into play as we were building out the programs took us some time and we were really diligent and thoughtful about how we set that up. So looking forward to our conversation here today.

My background is in financial services, so I worked for large global financial institutions. And most recently prior to joining up and working with the team to start MoXi, I had the fortunate opportunity to think about changing the way that mortgage construct such as it's been for the last 100 years or so and adapting and evolving that. Why does it have to always be the same? And so changing the way that the mortgage construct is to solve new and emerging problems. And so I see this as another way for us to do that. And so why not make global home ownership possible for the world and for its people? So anyway, long introduction.

Kenda:

It really has made a difference. No. That's actually terrific because it really has made such a difference for the home buyer here. Because I'm familiar with Cabo real estate, but you do offer your services throughout Mexico, but Cabo is a very expensive place and we have people who are wanting to purchase properties in Cabo and they're very expensive, the properties here. So to just put down all of that cash can be pretty daunting, whether your budget is a lower budget or a giant budget. Not everybody wants to liquidate all their money and put all their money in a home. Can you tell us a little bit about some of the programs that you offer to purchase properties? Let's start with existing homes. Let's just start with a home that is already built and livable.

Alex:

Yeah. Absolutely. MoXi exclusively lends on residential product and what that means is condo, town home, PUD, obviously a single family residence or even a one to four unit property, but primarily residential. And in the example you gave, an existing residence that's a resale that's already built, it's being sold to a new buyer, MoXi will make a loan to the buyer. Oh, it's so great to see all these people joining and-

Kenda:

I know. It's fun, right?

Alex:

Leaving comments. So hello. Anyway, so MoXi will make a loan to the new buyer up to 65% of the lower of the appraised value over the purchase price. So it's a 65 LTV maximum loan, which requires the buyer to have 35% down payment, which is a little more than a typical US mortgage. MoXi requires a minimum 700 credit score and the buyer, in addition to the down payment, needs to have ... I know we'll at some point get to this question today. But the closing costs in Mexico are very different, so closing costs and reserves are another key component of qualifying for MoXi financing. And then the loan program that MoXi offers today, clients can choose a term. 15, 20, 25. Up to 30 years, so like a US mortgage. Fully amortized, made in US dollars, serviced in the United States. Closed in Mexico, but serviced in the United States and serviced in US dollars. No prepayment penalties today.

Kenda:

No balloon payments. It's a fixed rate.

Alex:

Fixed rate, fully amortized. We spread out the entire amount of principle over the selected term. Most clients opt for our 25-year product, but we go up to 30. Yeah. It's US look and feel for the most part. From a credit underwriting and funding perspective.

Kenda:

For sure. I definitely think it does feel very similar to a US loan. It is a little bit different. One of the things that I know I talk to clients most about is the time that it takes to go through the process. It is a little bit more stringent and it's a little bit more lengthy in the time period, but everything here in Cabo is lengthy. A minimal closing period is 90 days. That's how long it takes to close. And in the United States you can close in two weeks, but you can't do that here. And you said the minimum credit score was 700. And did you tell us the other benchmarks that you look for in the approval process?

Alex:

I will. So yeah, our minimum loan size is about $250,000 US. And so when you-

Kenda:

That's the loan portion.

Alex:

The minimum loan size. Correct. Which means property value. We're looking at lending generally on property values in excess of 350,000 US. If you do the math exactly 250, 65%, it would be like 385. But generally we work with clients with a minimum property value of 350 and up. Meaning sometimes we'll make an exception to go a little below the 250. And then we lend all the way up to $2.5 million US. So sky's the limit on the upper part of the property value.

To your point around the elongated escrows, the credit approval process at MoXi is relatively quick. We've spent a lot of time building technology to make the process really streamlined, let's say. I almost want to use the word easy, but sometimes it's not always easy. So we've worked really hard to make the process as seamless as possible on the upfront credit side. And so our team is really, really skilled and seasoned in that area. So we can offer pre-approvals either fully underwritten or just based on stated income and a credit report and we can turn those around relatively quickly. It really depends on how quickly the client is able to upload the documents we request into our secure portal. But that can be done in as few as 24 hours.

Where the rubber meets the road is really in the legal closing area. And one of the things I think people really appreciate about MoXi, and I know appreciate about working with a really seasoned agent like you, is the diligence with which we look at and help clients. Especially foreigners who are not familiar with the process in Mexico and in Los Cabos specifically, how we're looking at and evaluating the collateral. At the end of this, are you going to actually own it? Will anybody down the line be able to just show up and say, "Hey, that's actually my land that your house is sitting on," and so on and so forth. And so that level of diligence is really critical and I know a lot of clients enjoy working with us for that reason and with experienced professionals like yourself. And I think that's a really important point to make. And that ultimately when you do it the right way, that's where you see some of those extra timelines come into play. I would generally say, or advise people, if anybody's telling you, "Oh, you can just DocuSign close and you can close an escrow in 21 days in Mexico," that's a red flag.

Kenda:

Yeah. That's a big red flag for sure. Absolutely. I think the takeaway that I'm getting is even if your budget is like say 400,000, you can still, if you can't find anything that you like in that 400,000 budget price point, with a MoXi mortgage, you can be looking up to, I don't know, 650. I'm not doing a general math in my head. And then the second-

Alex:

Looking up to a million, right?

Kenda:

Yeah. Exactly. And then the other option is if you have a $6 million budget or a $5 million budget and you don't want to liquefy all of your funds, you want to be able to leverage your funds, you can also do the mortgage and only put down the 65% and finance the other 45%, so I think that's a really good way to help.

We have a couple of questions that are coming in, so I'm going to start with this one. This is from Ross and it says, "If we can get a MoXi letter, say from Schwab, that we cal pay the mortgage payments from a qualified retirement plan, is that acceptable versus a traditional mortgage underwriting with a credit score of 800?" That's a very specific question, so I don't know if that's something we could answer on this call, but-

Alex:

I think I'm picking up the intention behind this. It sounds like ... Well, let me use a general underwriting discussion topic here. So can you use qualified retirement income and/or draws, for example, from an IRA or a pension or 401k, can you use that as income to qualify for a mortgage from MoXi to buy or refinance a house in Mexico? And the answer is yes. So if you receive a pension, if you receive social security, if you are taking required minimum distributions or even more than required minimum distributions, we can use that income to help you qualify for a loan at MoXi. A lot of people that are over the minimum age to start taking draws from an IRA set that up on a monthly ACH where it comes out of the IRA account, the securities are liquidated, it goes into your checking account. If we have proof of that agreement where that money is going in and two payments worth ... So two bank statements showing it's come in. I think one or two. We'll use that as income to qualify for the debt. I think that's what the question was.

Kenda:

It is. And he says thank you. He says that's exactly what he needed, so that's great. And we have one other question I want to ask really quickly and then I want to get back to talking about different types of properties that you will cover. But Carmen is asking, do you offer loans for new builds? Which was a nice segue into my next thing to ask you. What about pre-construction or new builds? What do you do? And also she's asking specifically about Quintana Roo.

Alex:

Yeah. Great question. Hi Carmen. So yes, MoXi does lend on new construction and we generally lend across Mexico, so most markets in Mexico, whether that's in Quintana Roo, whether it's in Baja Sur, whether it's in Mexico City. Anywhere and everywhere, for the most part from a collateral standpoint, we will lend subject to certain aspects of our credit policy. With respect to new construction, regardless of which market it's in, whether it's Quintana Roo or any other state, with respect to new construction, we will fund the loan when the deed transfers because that's how we get the lien security. So what's special about MoXi is that we can lend in US dollars to US people and secure the lien instead of with some asset in the United States with the actual asset in Mexico. So in order to make the loan, we have to have collateral. And so MoXi absolutely can make a loan on new construction and we do it once title transfers from the developer to you, the buyer, or to the borrower.

And so there are a couple of Mexico specific items that are required in order for that to happen. The developer has to manifest the construction. Essentially tell the tax authority this was a vacant plot of land and now it has a house on it or a condo building. And it takes a couple of weeks and the developer is responsible for doing that. The big long tent pole, so to speak, is the condo regime. So if a condo regime is applicable for the specific collateral, that has to be filed with the public registry. The developer is responsible for doing that. And the timeline for recordation of a condo regime can be in the months. So some developers will do early occupancy, give you the keys, there's still some small amount left of your deposit. MoXi will still lend up to 65% of the value of the house, and you would just get that back at closing. So if you only had 10% left in your contract, you take out the 65 LTV loan and there's an overage in the escrow account, you get that back to replenish the deposit you made to the developer. Hopefully I didn't lose anyone here because it's a bit complex. But short story, yes, we lend on new construction but not until title transfers.

Kenda:

Yeah. And I think it is complex because it's complex how it works here. It's just different. It's not complex, it's just different than what we're used to. But that's a really key point. If you buy a lot or you buy land and you want to build your own house, that's different because you can't get the lending on the construction. Is that correct?

Alex:

Correct. MoXi won't lend pre-construction.

Kenda:

A construction loan.

Alex:

Because it would effectively be unsecured debt at that point. We will lend when the collateral is there, so when the closing occurs, and clients can get those funds back. And I would just say high level here, if you are in contract to buy new construction and are thinking about buying new construction, it's a very popular choice. And there's so much development happening in Los Cabos, in Quintana Roo. Make sure you have a good team behind you. So work with an agent like Kenda or someone on her team, work with a firm like MoXi or hire a really good lawyer. Just make sure that you are going in eyes wide open so you understand some of these complexities. Maybe not complexities, some of these nuances that are really important.

Kenda:

And we just got this message from Hugh, I think. "I'm doing a new construction and paying out of pocket. Can you refinance once the construction is completed?" I think that goes to what you were just trying to specify there. Is that correct?

Alex:

And the answer is yes. MoXi is, as far as I know, one of the only lenders that offers refinance and cash out refinance. So if you bought your property a couple of years ago, you want cash out of it for any reason, we can help with that. If you bought vacant land, you already built something, it's now manifested, you can absolutely take out a refinance or cash out refinance to use the proceeds for whatever you want, including replenish construction funds. And then if you're buying new construction from a developer, you'll want to apply with MoXi like 90 to 120 days before the actual closing.

Kenda:

Closing.

Alex:

Otherwise you'll pay notario fees twice. Fideicomiso set up twice.

Kenda:

And Stacey asks basically the same question. The home equity loan for houses that were originally paid for in cash. And then Skandan basically says the same thing. "We have a mortgage from MoXi. If we pay it off, can we get a line of equity from paid property to purchase another property?" That seems to be a pretty popular question.

Alex:

Yeah. And the answer is absolutely. We do offer refinance and cash out refinance mortgage loans. Meaning a home equity line of credit such as it exists in the United States doesn't exist in Mexico. So when MoXi originates a mortgage in accordance with local law, with Mexican law, there is not a lien type that exists to be able to offer a variable principal balance credit line, so it is a one shot. You could think of it as a home equity loan. But it's a first position lien mortgage that we offer refinance or cash out refinance. First of all, whomever this is that is a current MoXi client, thank you so much for working with us. We appreciate you. And if your value increases, for example, and/or over time you've paid down the principal balance, you absolutely can refinance. We would pay off the existing loan you have, give you a little extra cash out and you would end up with one new loan as opposed to a primary mortgage and a second, if that makes sense.

Kenda:

It does. It does. I think that's a great answer. And then we got a question from Denise. She's from Los Cabos and she says, "Is the interest rate different to purchase versus a cash-out?"

Alex:

Yeah. Very good question. Hi Denise. It's pretty much the same. It's maybe slightly higher, a few basis points higher or something like that. Nominal difference. More or less it's the same. What I would suggest though, if you are working with an agent or if you're already in contract, you should reach out to the MoXi team now because if you can do the purchase money mortgage versus waiting and doing the cash-out ... When you think about that, you think in the US it's very common. Oh, we'll do delayed financing. We'll close in cash and then we'll just do a refinance immediately afterwards. It's a little different in Mexico because of the recording time. MoXi can't process refinance or cash out refinance until the original purchase has recorded with the public registry, and that can take months. Plus you have to pay notario fees twice and you have to pay the fiduciary fideicomiso setup fee twice. So if you are currently in contract, reach out to us right away. We'll do everything we can to try to meet that date. But if you've already closed, absolutely. We would just wait until the final deeds are recorded, the public registry, in order to move through the collateral processing part of the mortgage at MoXi.

Kenda:

That's terrific. Sorry, I have a call coming in. We're talking a lot about the timing of when you do things. One question that I get frequently is, "I'm coming down to Cabo to look at property. How far in advance should I pre-qualify with MoXi?" What is your recommendation for that?

Alex:

Yeah. It's really a personal choice for the client. MoXi offers two levels of pre-qualification. One is a full credit application, a small application fee to pay to pull a credit report, and then some basic documentation around income and assets and we can give you a MoXi match letter. The other option is a fully underwritten. So you're going to upload all of your taxes, all of your assets statements, and it's going to go to a member of our underwriting team and be manually underwritten and you get out of that a conditional loan approval letter that's many pages long. Very, very robust, I would say. And those generally ... A credit report is valid like 90 to 120 days. So if you really are not sure you're going to qualify and you want to get that taken care of in advance, we absolutely do that. We do it every day and we're happy to.

If you are just starting the conversation and starting to look into it, maybe you want to do your initial shopping first. But if you're pretty serious, by all means, do it. If you do the fully underwritten approval and then you immediately get into contract, half or three quarters of the work from a credit underwriting perspective is already done. So it's very easy. You upload at that point your contract, we make a couple of changes in our system, you pay your initial credit decision fees so we can order the appraisal and title and those kinds of things and we're off to the races. A lot of the harder work is out of the way. But again, it expires three months after you do it.

Kenda:

And from a realtor perspective, I've seen situations where people fall in love with a property and they did not do the free qualification and it's above their budget and that's a stressful situation from my perspective, so I always try to encourage people when they're sure that they're ready to buy and the time is right that they go ahead and do that pre-approval.

Alex:

Yeah. I would agree-

Kenda:

I think that gives us an idea of what they might be approved for.

Alex:

I would definitely agree with that sentiment. There's absolutely nothing wrong with it. And that we do offer those two choices, two paths. Totally.

Kenda:

Okay. Yeah. Lew would like to know if more than one person is on the loan, will that help them qualify for a larger loan amount? So if you have a joint income couple, does the joint income create a better opportunity for a higher threshold?

Alex:

Yeah. Great question and I'm going to couple it with one of the other questions below. Can you use Airbnb or short-term rental income to qualify? The answer to both of those questions is yes. One important thing to keep in mind. At MoXi, and I think in general ... I think this is law driven. The borrowers on the loan must match the deed. The recorded deed. So you can't have a non occupant co-borrower, for example. You can't have somebody signing on the loan just to help you qualify for more, but they're not actually vested on the deed. MoXi does allow vesting in US based trusts, LLCs and corporations. So that's not an issue. You can create an entity in the United States and put whomever you want into the entity, but each of those physical people must be borrowers on the loan and each borrower on the loan must be on the deed and vice versa. So it's important to just keep that in mind but absolutely.

With respect to subject property rental income, you absolutely can use it to qualify. However, there has to be some documentation for that property. So on a refinance, of course. You can upload your Airbnb statements. You already own the property, you're already working on it. No problem. If you are purchasing a property that has a historical documented history of receiving that rental income and you can get those records, we can use them in the overall picture of the underwriting conversation. But if you are just thinking about renting it and maybe you've done that before with other properties in the US, in the United States, you can order a specific type of appraisal that gives you projected rents. There is no such appraisal in Mexico, so unfortunately if you're buying a house that has never been rented before, in Mexico, we can't use subject property rent because there isn't anything to use and the appraisal will not include any projected rental income.

Kenda:

Yeah. Okay. Bill wants to know estimated closing costs. Closing costs in Cabo are high. You do have to pay a specific tax. It's an acquisition tax called an ISABI tax. And that is a tax that is charged to you in full at the time that you close. And so that tends to make the closing costs a little bit higher. The ISABI tax is a 2% tax on the purchase price of the property. So depending on the purchase price of the property, that 2% can be a significant amount. However, that's offset by the fact that our property taxes are much, much lower than they are from my experience in the United States. So you pay a little bit more upfront in the taxes and less annually. But I think most closings depending ... There are so many different things that qualify to make a different closing cost, but really I think you can safely estimate between five to 9%. Don't you think if there's lending?

Alex:

I would agree. And I'm glad you said that. Depending on the price of the property you're buying ... Because there are some fixed costs. Like a notario charge is going to more or less, the honorario portion of it is more or less going to be a flat amount. But that's a lot. 9% closing cost is a lot compared to a US. You absolutely should budget for that nine, 10, 11, even 12. If you're buying a lower priced property, you should plan on double digits and it is significant. So I think it's just important to really keep that in mind. It always sounds really exciting, but there is a lot of value to your point. So much lower property taxes, much lower overall cost of living, even in expensive markets like Los Cabos, lower property insurance premiums and so on and so forth. So I think there are a lot of offsets to that, but it's definitely important for buyers to remember that. Not significant upfront costs and charges.

Kenda:

Yes. For sure.

Alex:

When we quote seven to 12% closing costs, we're including all third-party fees, costs, and charges, and there are a lot of those. There are a lot of third parties involved in doing a closing in the right way. And MoXi has a pretty dense but great fee disclosure that we share openly with our clients that details out, of course, all of our fees. But really the second page of that sheet is this one long page of all of the potential third party fees, costs, and charges.

Kenda:

But I do appreciate the transparency because most clients tell me, I would rather just know. Just tell me the worst case scenario. I don't want any surprises. So it's nice that you have that transparency. Adrienne's asking, can you loan to US expats? The US citizens who earn income overseas and file federal taxes in the US? So if they earn income in Mexico, none in the United States, they only earn income in Mexico. Can you do loans for them as well?

Alex:

Yeah.

Kenda:

That's a great question.

Alex:

It's a great question. So in the answer I would have to ask probably more questions. But the answer is yes. We'll use federal filed personal US income tax returns to calculate income generally speaking, and we do allow the use of foreign income to qualify for our mortgages. So generally, yes. If you file us personal federal income tax returns and you have a credit score from all three US credit bureaus, you're probably a good candidate for a MoXi loan. We will leave it at that. If you're a US citizen as well, or if you're a US permanent resident, you could also be a permanent resident in Mexico. That's totally fine.

Kenda:

And then this brings us to the next question about Canadians and the mortgage guy is asking about that.

Alex:

Yeah. So great question. MoXi doesn't finance properties in Canada. We exclusively finance properties in Mexico for now. And MoXi exclusively lends to US citizens and US permanent resident aliens. If anyone from the MoXi team is listening to this, you're probably chuckling into your computer screen right now because we get the question a lot. Probably multiple times a day. Today MoXi doesn't lend to Canadians or in Canadian dollars. It is on our future state roadmap. We get the question a lot so stay tuned.

Kenda:

Perfect. Yeah. Hugh also wants to know, is there a base calculation on what MoXi fees will run for a refinance loan?

Alex:

Yeah. Okay. Good question, Hugh. So again, really, I would say ... It's a big range. But five to 12% closing costs in mind on a purchase. It's going to be lower on a refinance in a couple of ways. One, you're not likely going to have to pay transfer tax unless you're changing the vesting of the entity. I don't want to get too complex here. But you're not going to have to pay transfer tax in most cases on a refinance or cash or refinance. The second part is a lot of those costs will be netted from your proceeds at the end. So you will have to pay upfront for your title search, for your appraisal, for your manifestation if you need one for the legal work. And probably the notario will require you to wire half of their fee. But any remaining fees, cost charges, including funding your impound account for property taxes and so on is all netted from the proceeds of your loans so you don't necessarily have to come out of pocket with it. And closing costs will be generally lower on a refinance or cash or refinance because you're not paying the transfer tax.

However ... And I know that that might seem a bit contradictory to what I mentioned before. If you're in the middle of a purchase transaction, you're better off doing the loan now as opposed to waiting to refinance. You'll pay the ISABI tax either way, but you will save the notario fees, the recording charges, and the fiduciary setup if you do it right upfront.

Kenda:

Okay. Thank you. If you sell your property before the loan is paid off, can that loan balance be transferred to the new owners?

Alex:

Good question. So most MoXi loans are not assumable. If you sell your property in the closing, the loan would get paid off and the lien would get released during that process. The new buyers are welcome, of course, to apply and get a loan from MoXi and we can run those two transactions concurrently at the same time. But generally the loans are not assumable. There are some provisions in the event of certain things. Contingent beneficiaries and so on and so forth. But generally in a arms length purchase and sale, they're not going to be assumable.

Kenda:

Okay. Great. Ross follows up with his original Airbnb question and is asking, what about existing Airbnb rental resales? Can you use the past rentals experience to help qualify? And I believe you did say yes, you can as long as it's documented and it's for a sizable time period.

Alex:

Correct. Yep. That's absolutely correct. Generally, it is an additive part of the ability to repay underwriting calculation. It's not exclusively so. DSCR loans is not a MoXi program if that's where some of these questions are going. We're going to underwrite the borrower or borrowers. The subject property rental income would be an additive portion to help maybe with the debt ratio or help you qualify for more, but it's not a DSCR loan, so I just want to make sure everyone's clear about that.

Kenda:

Yeah. What do you think about Dyllia's question here? American citizen 20 years old, no credit history, can they get a mortgage with a Mexican co-signer?

Alex:

From MoXi, the quick answer ... I like to just be very transparent. The quick answer is no. So we require that you have a valid credit score from the US and eligible borrowers at MoXi are US citizens or US permanent residents. So a Mexican co-signer wouldn't be a permitted borrower in any case, whether it's a co-signer or a primary borrower at this time.

Kenda:

And it's difficult to just say that, but that's how it is.

Alex:

But you could work on that credit history. I think it's three trade lines, three active trade lines in order to not have thin credit files. So be very responsible, but you could establish some history and we'll talk to you in a couple of years, maybe even-

Kenda:

Couple of years.

Alex:

Yeah.

Kenda:

Yeah. That's always fun to go through that process and to remember back when we were starting off and how it's something you just have to go through. And she's asking what if it's an American co-signer? I think it's really not even so much about the co-signer. It's about just the lack of personal credit history. Is that right?

Alex:

Yeah. The term co-signer is an interesting one. But if it's a borrower ... So non-occupant co borrowers are not allowed in their MoXi programs, but if it's two people wanting to buy property and use a MoXi loan to do it and the combined total amount of income between the two and or assets fits within the guidelines, it's no problem. So you could have a second person. We're going to use the primary wage earners, middle FICO score to score the loan. So if there is a second borrower that's maybe not contributing on the income side but is going to be in the deed, and so they're going to also be a borrower, those are situations we can definitely look at.

Kenda:

Okay. David asks ... He got approved by MoXi a few months ago. And we also had this question ... It was one of the questions that was asked earlier in the week. We had an ability for people to leave their questions ahead of time and this question was asked. So let's talk about how long that pre-approval, or I guess maybe he says he got approved a few months ago. How long does the approval last?

Alex:

Yeah. Great question. So it lasts as long as the documents submitted for the approval are still valid. And generally most of those documents are going to age out around 90 to 120 days. So three to four months. We can always update that approval. And if you're actively shopping, I would definitely stay in touch with your mortgage advisor, stay in touch with us and let us update that approval for you. The credit report can be refreshed and re-polled if you've had any significant changes. But if you have done a full approval with us and we've looked at your taxes and you know haven't had a lot of changes, like you haven't leased a new fancy car, bought a new house so there's not a lot of new debt on your credit report and or your income is stable and or your assets haven't really changed, you can feel generally pretty good about that. And when you do get into contract, we can refresh things, but if you want to keep-

Kenda:

Is that an additional cost, Alex?

Alex:

Generally not. If we have to submit the loan back to underwriting, it's a whole new underwrite. So it is. But if it's a refresh maybe, like a new credit score, just updating that, I don't think there's any cost for that. Maybe you need to upload a new pay stub or something like that. But again, I would say if the approval was given, depending on what approval we've given you, the approval is given and nothing's really changed about your situation, we can certainly stay in touch and tell you if anything changes about our credit underwriting guidelines. But if nothing has changed on either end, you should feel pretty comfortable. If you're getting ready to go put in an offer, that would be the time to come back to us and have us re pull your credit and check that out and just make sure everything's good.

Kenda:

One of the other questions that we got ahead of time, which I thought was really interesting is we had a current MoXi customer who is selling their property and the people to whom they're selling their property want the clients to pay off the loan before getting to the closing table. And they asked if that was customary or how the payoff works. And basically we've had this situation ... And just to clarify, MoXi will be given their payoff funds at the closing table. It will be distributed from the escrow account and it will be sent and then will be paid off at the closing table. Now, many people who have Mexican bank accounts, so many Mexican citizens who are used to the Mexican bank account, you do have to pay it off before the closing table. So the person who was asking, why is my buyer requiring this? This might be a Mexican buyer who is thinking of the Mexican bank regulations as opposed to somebody who understands that this is a different type of mortgage. So just have your agent or just explain to them or have somebody called MoXi. I don't know what you need to do there, but that is not typical. Typically, with a MoXi loan at the closing table. Money is dispersed from escrow and that is what fulfills the MoXi loan at that time.

Alex:

Yep. And I would say somebody, a current MoXi customer is selling their home, you probably have counsel. You probably have a lawyer that's helping you. That would be an important question. Or we can always give a recommendation of counsel that can help you. But just the same way as you're buying a house in Mexico, you'll want to have competent representation. I would recommend the same as if you're selling a house. It's not an overly complex situation, but you want to make sure you're cared for. There are capital gains taxes. There are all sorts of different considerations beyond just the payoff of the MoXi loan.

Kenda:

Yes. There are so many moving parts and important things that you really do need to work with a very experience professional when selling your property whether you have a loan or not for sure. One of the other questions we got was can I obtain financing if I have dual citizenship?

Alex:

Yeah. So good question. And this is a really interesting one. I love all these questions because they. Are things that we have sat around the table about proverbially or actually and worked through in the past four years or so to make sure that we have a credit policy that aligns to that, that we can address some of these questions. So anyway, I really appreciate them. The more detailed the better. It's fun.

So yes, dual citizenship is permitted. From a MoXi credit policy standpoint, we lend exclusively to US citizens, US permanent residents. So so long as you get that criteria, you have a credit score from all three bureaus and you file US personal federal tax returns, and you make them available to us even if you're doing a bank statement loan, we still are required by Mexican Law to retain copy of proof that you're a US taxpayer. That's all fine and well.

When you get into the legal property transfer side of this, MoXi is going to secure its lien for the mortgage using the Fideicomiso de Garantía, which is like the trust agreement. The Fideicomiso itself was designed in part through an amendment to the Mexican constitution in the 90s. And it is specifically for foreigners. So if you are a Mexican born US citizen, your passport, your US passport says birthplace Mexico, there is a possibility that when the fiduciary goes to submit your permit application from the Secretary of Foreign Affairs, there's a possibility that they'll ask for a copy of the passport and then they'll say, well, how could you be a foreigner if your birthplace is Mexico? And so there are some workarounds for that. And the main one is you take title in the name of your US based trust, LLC or corporation. That's the primary way that you get around that. Many clients choose to do that anyway so maybe that's something you're already doing. But if the buyer is a US entity, then it's a foreigner. So I think that's an interesting way to think about it.

Kenda:

Yeah. And that is a really detailed question and it seems like a simple question, but it's not a simple question. So I'm looking at some of the other questions that we received. How much is the down payment that's required to purchase a home? I think these are questions that you did a great job of answering. I think a few people want a job with MoXi. You have a few people who ask, are you hiring? Because this is such a great company. So I-

Alex:

I remember seeing that that one come in from our social. So I will say if you are a US mortgage professional watching this, if you're a US mortgage broker, we just recently launched a beta pilot of our broker referral program. And so we have a very defined process, and it is very much in test pilot beta launch. In fact, I probably shouldn't even be talking about it so publicly. We're piloting this right now where US mortgage brokers can refer clients to MoXi. So there is a certain amount of diligence we require of any broker that's applying for the program in the beta phase. So there is a link, we will post it. I'm hoping someone from the MoXi team watching this can post this here. And you can go and check out ... There's a video and some more information about that program on our website specifically for US mortgage professionals.

Kenda:

Okay. Perfect. And with a decent credit score, what is the average interest rate that MoXi's offering right now?

Alex:

Yep. Really good question. In fact, I'm surprised we haven't had it yet.

Kenda:

Me too.

Alex:

So MoXi, we have a risk-based pricing model. So it's going to be based on FICO loan to value the percentage you're putting down and or the loan amount versus the lower of the appraised value or purchase price, and then loan size. So the higher the loan size, the lower the margin is. And those are the three primary factors. There are what we call loan level pricing adjusters, LOPAs that are also added on top. So for example, if you have a credit policy exception written in, there's a price up for that. If you're in an area that does not have title insurance and we have to use a legal title opinion instead of title insurance, there's a small price up for that. There's a couple of other purchase adjusters. All of that said generally, so in our rates are priced based in the US three-year treasury, which changes minute by minute. It's changed 35 times since we've just been on this conference. So generally you can expect a rate about one and a half to two points higher than the prevailing US 30-year fixed mortgage rate might be. So for MoXi clients that are closing today, there may be ending up in the mid to high eights to low 10s would be my guess. Again, lower the loan size, the higher the interest rate's going to be.

If the property is in an area that doesn't have title insurance, it's going to be a little bit higher. If the FICO score is lower and or the down payment is less, the rate's going to be a little bit higher. So it's going to be in that range.

Kenda:

How does the currency affect the mortgage. The different currency exchange rates?

Alex:

Yeah. Great question. So by design MoXi's programs don't subject our clients to foreign exchange risk generally. Because the loan is made in US dollars, even though it's secured by Mexican collateral and the interest rate is fixed. Once the loan closes, the interest is fixed for the entire term. MoXi does not lock interest rates until we finalize the interest rate about 48 hours before you're closing. But we disclose all of this in the conditional loan approval letter. So based on the anticipated LTV, your FICO score, the property you're buying, you'll know exactly what your margin is over that three-year treasury, and you can track it right on our pricing page. And then about two, three, four days before you close, the rate will be finalized and that you have that rate fixed for the entire term up to 30 years.

Important to note ... We just saw that question about the fees and insurance. I will say one of the things that makes MoXi special is we don't require life insurance for our loans. And if you're from the US you're like, well, of course you wouldn't require life insurance for a mortgage. But in Mexico it's a thing, but not with MoXi. So we don't require life insurance and we do not require mortgage insurance at all either.

Kenda:

Okay. And David is asking, can you purchase property before getting a Visa? I assume you're referring to maybe being a permanent or temporary resident Visa. Not just a travel visa. And yes, you can purchase property in Mexico without being a permanent or a temporary resident. There are benefits for you if you become a temporary permanent resident, but they have nothing to do with the ability to purchase a property. So hopefully that answers your question, David, I'll let you tackle this one from Ross.

Alex:

Yeah. The first part of the question would be my standard [inaudible 00:54:40]. We are not tax advisors, we're not CPAs. Clients have reported to us in the past that because we report mortgage interest paid to the IRS via a 1098 INT. Clients have reported historically that they've been able to turn in that 1098 INT to their tax advisor. And there is generally some benefit to the mortgage insurance. Excuse me, mortgage interest. Because the mortgage interest is being paid by you on a second home or investment property. And so that interest is reported and can theoretically be considered for deduction. I'm not even going to say deducted because I don't know. And you really do want to talk to your CPA and or a competent tax attorney for that question. We also get questions a lot around 1031 exchange. The simple answer is it's like for like. So if it's a US property, that's investment it can't be a Mexican property, that's investment. But if it's Mexican property investment to Mexican property investment, it can. There definitely are some tax things and I would definitely encourage you to talk to a competent qualified professional in that area.

Kenda:

And I would piggyback on that and just say that it might be worth looking at an international tax advisor because some tax advisors in the United States don't really understand all of the laws with other countries and the ramifications of having properties in other countries. So it's always better to get an international tax attorney to answer those questions. So we are about out of time. So Hugh there not mortgage insurance fee associated with a MoXi loan. So that's I think hopefully the answer to that. That's correct right, Alex? You just stated that just a second ago.

Alex:

Yeah. No mortgage insurance. MoXi does require title insurance where it's available. We arrange and coordinate that. And then we do require property insurance. If anyone's watching, don't buy a property without insuring it.

Kenda:

Absolutely.

Alex:

That's my general advice.

Kenda:

Absolutely.

Alex:

But yeah, you got to have hazard insurance. There are many.

Kenda:

You have to have this and liability for sure. Well, Alex, one of the questions we got early on that I waited until the end to ask is how do we contact MoXi? How do we get in touch with MoXi if we want to get more information, more specific information? Is there a contact person in Cabo or in Mexico City or do we just reach out to you online? How do we get in touch with somebody to start the process of getting a loan approval or even just more information?

Alex:

Yeah. Great place to reach us is through our website, so www.MoXi.global. No dot com. Just dot global. And that's a great way. There's a lot of information, a lot of FAQs on our website. We have a mortgage estimator, a mortgage calculator, as far as I know, first of its kind that lets you estimate a Mexican mortgage. And there's a link to that from our main page. So again, www.MoXi.global. And from there you can submit a contact test form to talk to one of our mortgage advisors. We have a special tool called the MoXi match tool. So you can self-serve and get some general information about whether or not you're a fit from MoXi financing at this time. So answer questions like, are you a US citizen or permanent resident? Do you have at least 35% saved for your down payment or your existing owner in your refinancing, it'll ask you questions based on that path. And then it will let you know if we think you're matched, if we don't think you're matched, will send you an email. You can reply to the email and say, I am a candidate and I do want to have a call.

So there's a lot of cool tools on our website. It's a great place to start. Our YouTube channel has a lot of videos. I'm in some of them. But our great fantastic MoXi team are also in a lot of them. And we tackle everything from how do we look at credit underwriting and income to what is a manifestation of construction, a condo regime, how do closings work in Mexico? I think that's a great resource as well. But we're always happy to help. This is all we do. We love it. And on behalf of the entire team, we're really looking forward to chatting with you and continuing to work with you, Kenda. It's just been so much fun getting to know you through this process as we've prepared for today and as well working with your clients and you personally. So thank you.

Kenda:

Yeah. Yeah. It's been great and I appreciate everybody who joined us today. I also have a YouTube page where I talk a lot about different nuances of buying property in Cabo, what life is like in Mexico as an expat. And if you'd like to find me on that channel is the YouTube channel called At Home in Cabo, and I share a lot of both real estate and just general lifestyle in Mexico. So thank you guys so much for joining us today, and we're so appreciative of your time. And if you have any further questions, please feel free to reach out to us in the comments. This will go posted on our pages and you will be able to watch it again and ask any questions that you have in addition. So thanks so much for watching, we really appreciate it.

Alex:

Appreciate you. Thanks so much, Kenda. Bye everybody.

Kenda:

You too. Thanks Alex.

Alex:

Thanks for your time and attention. Great questions. Bye now.

Kenda:

Thank you. Bye-Bye.

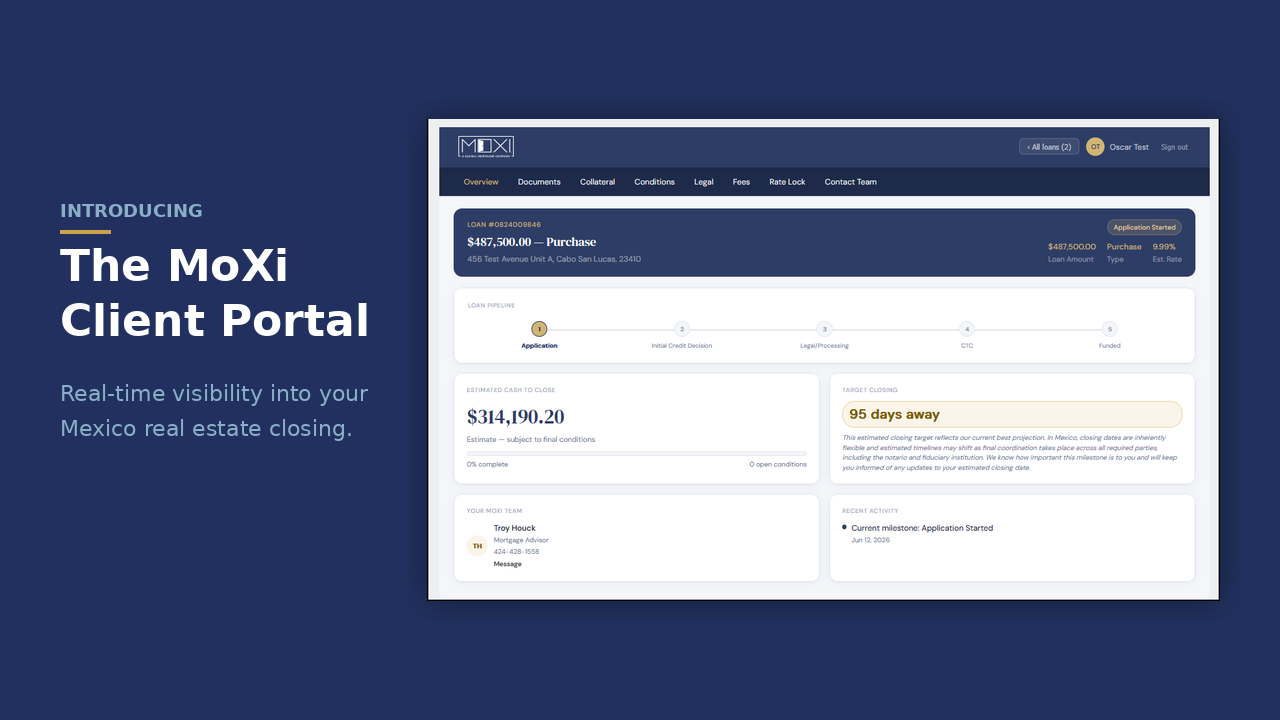

Did you know that MoXi funds & services loans in USD, is regulated and audited in the US & Mexico, and ensures compliance throughout the term of your loan?

Try our MoXi Mortgage Estimator