How To Finance & Legally Own Property In Mexico

Video Transcript - (with Chris Childress)

Chris:

Thank you everyone for joining us. Again, this will be our second session here in the last 30 days. Last time we did a webinar like this, it was a terrific turnout and just had wonderful feedback, so we thought we'd keep it moving. I'm Chris Childress. I work here at MoXi, a global homeownership company and what we do is we specialize in financing residential real estate in Mexico for US citizens. So, we are gathered here today to really just review what we offer and go through some scenario questions and inquiries that people had submitted. Before we get started, a couple of quick housekeeping notes. Just keep us all in line there. Everyone is muted right now, but we do encourage you to engage, ask your questions, give us feedback and responses through the chat. Feel free to submit additional questions as we work through this and if we have time at the end of the session, then I'll certainly field live questions from today.

All right, so why have we gathered here today? Well, over the last few years we've seen a massive surge of US buyers looking into Mexico. People are investing in vacation homes, retirement properties, investment properties to drive that rental income and there's even folks out there like myself and several of my teammates who have made Mexico their permanent home and have invested in primary residences down here. And the biggest question that we find when people start considering owning real estate abroad and fall in love with Mexico and all the beautiful things that it offers, the biggest question we get is, is there a way to finance the property or do I have to just dream and try to come up with all the cash? The simple answer is yes. With MoXi, now US taxpayers can absolutely finance residential real estate in Mexico, but the process is a little bit different.

We've worked hard to make it look and feel similar to what our US based borrowers are accustomed to in the United States, but there is a different process to make sure that we're protecting not only you as the borrower but also or your clients. If I have real estate partners on here with us or your clients and also protect the investor, the process is a little different. So, we got to make sure we do our diligence, we go through the right steps in order to protect all parties and involved. And to be quite frank, there's really not many who do that well and that's really where MoXi comes in. We're out here, we started in 2017 and our mission was purely to create easy to understand and familiar resource for US borrowers to leverage real estate in Mexico and we're incredibly proud of what we've done so far.

We're going to talk about who qualifies, what some of the key requirements are. We're going to talk about trust structures or how real estate or is vested or how foreigners hold title in Mexico. We'll talk about rates and some fees. We'll talk about some real world scenarios, cash out refinances, pre-constructions, always a big one that people ask us about and we'll plug in the holes all the way in between. Most importantly, we're here to answer you guys questions. We asked everybody to send in questions ahead of time and you delivered. We've got a good stack today to work through and then we've even got some overflow if we have the time.

The way we're going to format, it's like we did last time. I'll share the question on the screen with who asked it and then we'll walk through the answer in a clear and simple way so I can explain the results and hopefully increase everyone's understanding of what we're doing down here. Again, terribly excited to see you and excited to get started moving through this. Also, one last quick word about MoXi. We're always asked and a lot of times is it a bank? Is it a broker? Is it your dad's money? I mean, where's the money sourced from type of thing. So, I just wanted to kind of let everybody know, MoXi is backed by us institutional capital. We underwrite our loans using US standards. So, it's again, going to look and feel very similar to getting a mortgage loan in the United States.

We've built an infrastructure to make cross-border lending work the way that we think that it should through technology and resources and we believe that to be transparent, reliable and borrower friendly. So, each year we improve our processes, we improve the customer journey, make it easier to understand and easier to navigate and we're again very proud of what we've accomplished and looking forward to continuing to improve. What we are not, we are not a Mexican bank, we're not a mortgage broker, we're not trying to find a source for each and every loan that we have. We've got that covered. We are a very well-funded mortgage lender that brings us style financing to the international market in a way that's designed to feel familiar, straightforward, and trustworthy. We've got a saying here at MoXi that we think owning real estate abroad should be exotic, not the mortgage you used to do.

So, we try to, even though there are some complicated pieces of the process, it is our goal to make it look and feel familiar and comfortable as we navigate through. So, let's get started with the questions. Kind of broken it up into sections here today, some of the questions. So, we'll just touch on some of the questions that come in and I've tried to group them together. There is some crossfade if you will, where the questions are overlapping with each other through the sections, but I do hope that with the questions we've selected that today we'll be able to help everybody have a clear understanding of exactly what it is that we're working with. So, let's start with the basics, how to apply, who qualifies and what options are available. Okay, question number one. Sonia asks, "How do I apply and what documents are needed?"

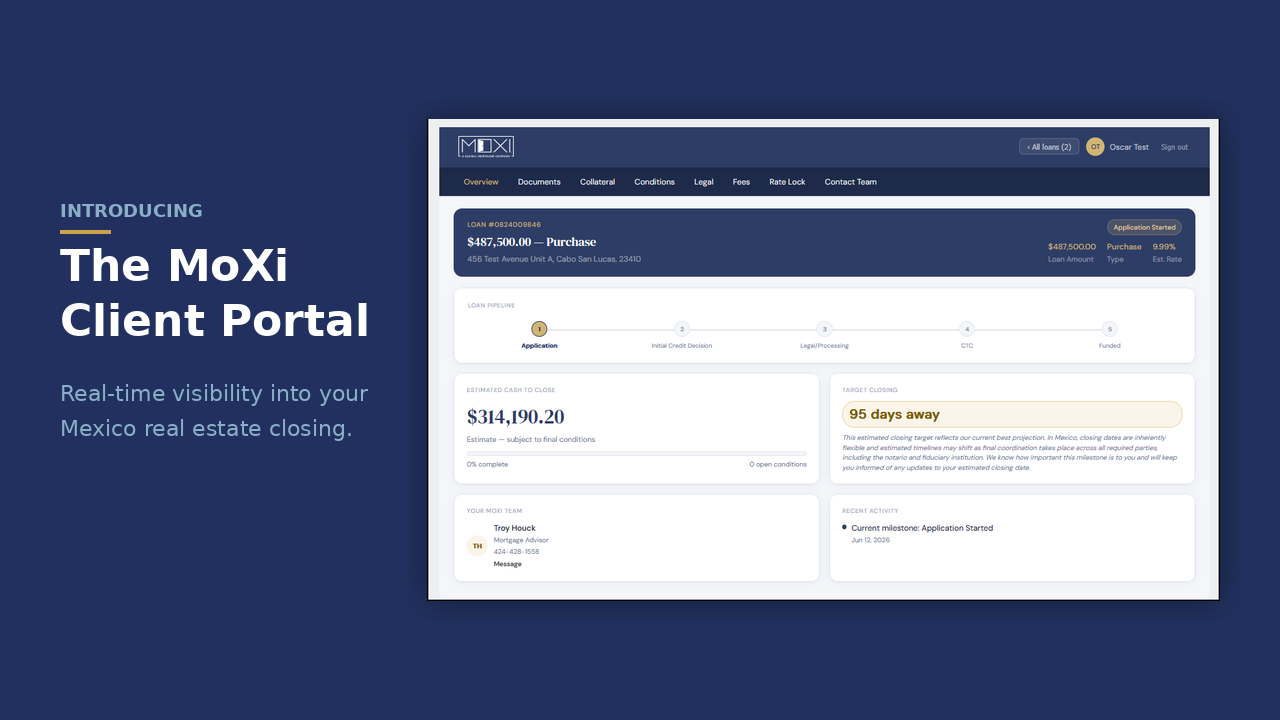

If you've ever applied for a mortgage in the United States or have any familiarity with that, it's going to look and feel very, very similar. We have a secure online loan application that lives on our website that is MoXi.global. If you're working with a mortgage advisor already or if you're not already, we recommend you get connected with one. Your mortgage advisor can also provide you a direct link to where that application will move directly into their queue so they can take care of you. But when you go to apply, it's going to look and feel almost exactly like it would to apply in the United States. We use the same technology, the same secure portals. The loan applications are very similar to what you see in the United States. Naturally we've had to incorporate some of the elements that are specific to the Mexican collateral, but at the end of the day it's going to look and feel very similar from an application and filling out the process there or filling out the application to get started.

And then once you submit your loan applications, we're going to respond and request basically the exact same things that you would get from your mortgage professional back in the United States. You're going to get a set of disclosures with some information on how the process works and that would also give [inaudible 00:07:53] for us to go to work for you to verify employment and income and work on your behalf. And then as far as documents are concerned, we're going to collect the same income and asset documents that you would expect to deliver in the United States. We like to call it the two, two and two here internally for a little industry language that's going to be your most recent two years tax returns or proof of income. If you're self-employed, we'll have to get some business returns and that kind of stuff in there as well. Your mortgage advisor can give you more granular details on that.

We'll get your most recent two months bank and asset statements so that we're able to document your source of your down payment as well as any reserves that might be necessary after you close the loan. And then we're also going to collect your most recent, we say the other two is two pay stubs, but essentially your most recent 30 days pay stubs or most recent year to date profit loss statements if you're self-employed to cover your year-to-date income. So, essentially we're looking to take a good hard look at your last two years filed returns and your year-to-date income. We're trying to project what's going to happen over the next three to four years for you. That's how we underwrite the loan. And then of course we'll need to document where the money's coming from a down payment and reserve perspective. So, again, everything you're going to do the application and the documents provide should look and feel exactly like what you'd expected in the United States and we're going to ask for basically the exact same types of things.

Leisa asked today, "How you get approved for financing?" Well, the same kind of goes along with the question we just went over. First, you'll apply for your loan. We will respond by requesting some documentation and things to look at it. And then at the end of the day, the approval itself comes down to three key things. It's that's going to be your credit, your income, and the collateral of the property itself. Okay? So, with MoXi, in order to qualify, you must be a US citizen or a permanent resident of the United States. We like to say US taxpayers must have a credit score of at least 700, 700 will let you get a program with us for up to 50% down payment.

We require a 720 middle score or better in order to achieve our maximum loan to value, which is 65% or requires a 35% down payment. We'll also have to check those documents that you provide to us and review everything and make sure that you have the income to support the loan amount and again, the assets and the reserves to cover your down payment. But again, we're going to underwrite this loan just like we would a mortgage in the United States. Again, take a look at what your total income is, take a look at what your existing debt service is or what your obligations are and then obviously we're going to look at your credit history to make sure that you've got an acceptable payment history in the credit scores to qualify for a MoXi loan.

Jose asks, "Is financing available to Mexican nationals that live inside the United States?" Jose, that's a great question, actually, one we get quite often. So, let me see if I can unpack that for us here. So, MoXi specifically lends to US citizens and US permanent residents. Again, a US taxpayer. If you are a Mexican national, meaning you're born here in Mexico and you're living in the United States and you have been naturalized or a citizen there, or I'm sorry, a permanent resident with a green card, then from a citizenship perspective than you would qualify. What we don't have though is a program for foreign nationals without US residency status. So, again, the program is designed for US taxpayers and again, that's going to be a permanent resident of the United States, or I'm sorry, a US citizen or a permanent resident of the United States with authorization to work in the US and are paying taxes. So, hopefully that answers your question there.

We'll talk about eligibility and loan terms. We'll talk about things like what you need to put down, what rates might look like, how loans are structured, and then just some other scenario questions. So, we'll move into section two. Okay, question five comes from Claudio and Claudio asks or says to us, "I'm looking to purchase next summer. How do I know if I'm approved and how much can I get?" That's a great question and again, I commend you for starting early and starting to look early. We have a lot of clients that'll come to us after they're under contract or they're getting ready to make an offer that day and they haven't quite got their financial house in order. So, we find ourselves scrambling to try to help out in that scenario. So, I applaud you for getting started early and what I would recommend that you do is to reach out right away to MoXi.

If you haven't done so already, please submit a form online or reach out to us here and then get connected with a mortgage advisor so that we can submit your loan application and get you fully pre-approved before you start shopping. It all starts with a discovery call. So, when you submit your information to a mortgage advisor, they'll invite you to schedule a strategy session where you guys can talk about your scenario, talk about exactly what it is you're trying to achieve. We can tell you how our process is structured, talk scenarios with you and that type of stuff. And then we can help you to get a solid, fully underwritten pre-approval so that when you go and start shopping and are preparing to submit an offer on a house, you can do so with confidence. You know that you've got a loan in place to get things going.

So, I do recommend you start at least having the conversations early, but we would apply and get you set up before you get out there shopping and then guide you through the process to make sure we're ready to fund when you're ready to take possession of the home. So, we hope to hear from you and hope to move forward with you very soon. Okay, moving right along. We'll move to question number six and Matt asks, "What is the best percentage to put down?" Okay, that's kind of, well, it's a loaded question, not a loaded question, but there's a lot of different ways to answer that and it really depends on your specific scenarios, Matt, exactly what you're trying to accomplish and of course what works better for you in your particular situation. For a purchase loan, MoXi requires a minimum of a 35% down payment, which means we'll finance up to 65% of the property's value.

Remember, if we have a credit score between 700 and 719 or below 720 and just above our minimum, then we'll be capped at a 50% loan to value, which means that it will require a 50% down payment. Now, that's our max loan to values or minimum down payment thresholds, but we do have a sliding scale with regard to interest rates and whatnot, and basically the more you put down or the lower your loan to value, excuse me, then the lower your interest rate, so the more equity or more skin you have in the game, then the lower the interest rate. So, it's kind of a balancing and deal there and I would recommend that that you touch base with your mortgage advisor so you guys could strategize on exactly what makes sense for you, what's going to give you the payment structure you're looking for and all that.

For a cash-out refinance, we will lend up to 60% loan to value. if you're looking to take equity out, we can do up to 60% and we'll be talking more about cash-out finances here in just a few moments. Just a quick note here, the equity cushion, the reason we have lower loan to values is because that keeps the loan sustainable, protects the investor and allows us to build the product base and then of course protects you, the customer, from market swings in the area. So, hopefully that brings a question for you. Okay, thank you, Matt. For question number seven, we have a question from Taylor and Taylor asked, "How much down and what is the rate, what are the terms, is it fixed and what do we need to show to qualify?"

There's a lot to unpack in that question, so I definitely wanted to take this one because this covers several things in one fell swoop. Now again, 35% is the minimum down payment required for purchases with a credit score below 720 and above 700. Then that's a 50%. So, that's what would be required for your down payments. The terms are typically between 15 and 30 years. Guys, we have a 15, and I do touch base on this here, a little bit greater detail here in a few moments, but we offer a 15, 20, 25 and 30 year fully fixed fully amortized loan terms and our loan officers can talk to you about which term works best for you.

That's for our core product. And to qualify, just like we talked about before, we'll need to see income, assets, credit history, all the normal things that you'd present when applying for a mortgage in the United States. So, we just want to make sure that you qualify from a affordability perspective can support the payments with the income that's there, have a history of doing so with good credit and that from an asset and reserve perspective that you've got enough left over so that if you do see a rainy day, you can carry yourself for a bit. Again, recommend talking to one of our mortgage advisors and they can get you greater detail on exactly how these guidelines, pardon me, apply to your particular situation. So, Taylor, thank you so much.

The question says, "I don't want to be in a 30-year mortgage. Does MoXi offer shorter terms like seven, 10 or 15 years?" The question is, absolutely. Just like I was just now talking about, MoXi offers, I put both here. My apologies for the typo. We offer several terms. We offer a 15, a 20, a 25, and a 30-year fixed rate loans. We find that most customers who are working on our core product, and I'll expand on that here in a little bit, but we find most customers on this program will choose our 25-year term and here's why. Again, we offer 15, 20, 25 and 30-year terms the interest rates. Unlike in the United States, the interest rates for our 15, 20 and 25 year loans are going to be the same.

Our investor doesn't charge any adjustment or any price difference for those terms, so we don't add anything there either. So, your interest rate would be the same for a 15 year as it would be for a 20 or a 25 year. Our investor, however, does have a bit of an adjustment that they charge if you want to stretch out to a 30 year, which is about 30 basis points or about three-tenths of 1%. So, just over a quarter of a percent higher in interest rate to go to a 30-year fixed. None of our loans, our loans currently don't have prepayment penalties or balloons or anything like that. There's no prepayment penalty, there's no reason you can't pay ahead or pay down your principle if you'd like to do so on our loans.

There's no penalty to do so. So, what most customers find that since the interest rate is the same on the 15, 20 and 25 year term and there's no prepayment penalties or any exotic features that would prevent them from trying to accelerate their principal and pay it down quicker, that most customers will opt for the 25 year because that gives them the lowest interest rate available for their qualifying metrics and gives them the lowest mandatory monthly payment. So, the lowest mandatory debt service. So, if you're using it as a rent place or maybe not using it some months, you've got a lower mandatory payment in the off season. Then if you felt like you wanted to accelerate your principal when rents are high, if it's an investment or whatever the case is, that's what most folks will do. Again, we offer 15, 20, 25 and 30. Most customers choose a 25 year because again, that gives them flexibility of the lowest mandatory payment, lowest possible interest rate, and again, there's no prepayment penalties or balloons that prevent early payment or acceleration of the principle.

Tim asks, "Can I get a mortgage on a paid-off property?" Tim, absolutely. We consider that, if I understand your question correctly, we consider that a cash-out refinance. So, if you own a property that's free and clear in Mexico, MoXi can lend up to 60% of the appraised value with a 720 credit score or higher up to 50% for 700 to a 719. Many clients can use that equity for renovations, additional investments or other things that they need to do. Again, so we treat it like a cash-out refinance. I'll talk here a little bit about a HELOC and that type of thing. This is not a HELOC, this is a fully amortized long-term fixed rate cash out refinance that we offer for real estate that you own in Mexico. Refinances, obviously we need to make sure they meet all the guidelines from a vesting perspective, titling the collateral itself or the home must meet MoXi guidelines.

So, we'll certainly want to talk to you about the property and make sure that piece qualifies, but 100% we offer cash-out refinances and I recommend you schedule a discovery session with one of our mortgage advisors right away to get more details. Right. All right, making good time here. Let's move to section three and here we're going to talk about structure and process, how loans work, geographical coverage, we'll talk about HELOCs, we just mentioned that a moment ago. Refinancing scenarios, pre-construction, things along those lines where we lend. So, let's talk about these topics here and we'll start with a question from Damon. Damon asks, "What's the maximum amount of a HELOC that you could offer on a home or offer in Mexico? And also what about pre-construction?"

A HELOC is a home equity line of credit and it's basically like a credit line that you can use or a credit card if you will. It's not a credit card, but it's like a credit line that you can use with equity on your home in the United States. It functions kind of like a credit card though or like a revolving line because you don't necessarily have to draw the whole balance out. You might have a home worth X. You might have, let's say you have a HELOC worth a hundred thousand dollars, you don't necessarily have to draw it all out and use it all at one time. You just have a line of credit or access to that. And generally those are not fixed rate loans and the rates are calculated differently. So, it's a whole different type of product.

MoXi does not offer a HELOC in the traditional sense here in Mexico, what we do is a cash-out refinance, like we were talking about just a moment ago, you'll have to close the loan and we fund it all at once and it's amortized over the predetermined term, but essentially we'll appraise the property, determine the value, we can loan up to 60% of the value of the property in a cash-out refinance loan. And that's what many of our customers are doing down here in Mexico in lieu of a HELOC. Again, we don't offer the traditional HELOC. And the second part of your question asks about pre-construction. MoXi does not currently have a construction product. What we're used to the stage funding where we can fund as we build and fund as we add to the construction, but we can fund once the home is complete and ready for legal transfer or legal delivery.

So, if you're working with pre-construction, which we have many, many customers that do, we will work alongside you to get pre-qualified, make sure everything's ready to go. We can't fund the builder along through the process. You'll have to make the deposit requirements in that, but once the home is completed and ready for delivery, then we can fund in that loan. If you've had to make deposits throughout the building process that are greater than what your down payment would've been using a loan through MoXi, say for example, they require that you pay a hundred percent before they'll finish the construction, right?

But you're only going to borrow 65%. So, basically you should have 65% of that money coming back to you. We can work it out to where you could be refunded that money when you go to closing. So, you would have to figure out how to support the payments and satisfy the obligations to the builder through the build process. But when we get to closing, then we can work it out to where you receive some, if not all of that money, back to you. Short answer, and I'd recommend you talk to a mortgage advisor to get greater details on exactly how that works. But the short layman's term way to think about this is that if as you make your deposits to your builder, we just consider those deposits to escrow when you get your loan approved with MoXi and we're ready to go to closing.

Just before closing, we're going to wire funds into your escrow account, let's say. So, what happens then is that creates a big overage in that account. You've put all your money in, so you've got all these credits now we've put money in that creates an overage there and then a refund would be due to somebody in a situation like this, Damon, that somebody would be you. So, we could work with you to try to strategize and make you whole as quickly as possible. We do not offer stage funding, again, but we can work with you to get you back funded as quickly as possible once you're able to receive legal transfer of title. Now, please let us know if that didn't answer your question or if I can clarify in any way. Okay, so our next question comes from Terry. Terry says, "How can you refinance to get equity from Mexico on a property that's already purchased and paid in full?"

We've been talking about that quite a bit today. Seems to be a lot of interest in our cash-out refinance or harvesting equity from real estate in Mexico here lately. That's exactly what the cash-out refinance does. If your property is titled and fully paid off and the construction has been what we call manifested or registered with the proper entities here in Mexico and the home meets MoXi's guidelines, then we can lend up to 60% of its current appraised value and put cash right back into your pocket. Again, looks and feels just like a cash-out refinance would back in the United States. So, super excited about asking in the inquiries regarding refinancing and cash-out refinancing here in Mexico. When we started MoXi back in 2017, there was just a void of institutionalized financing for foreigners.

I personally lived down here in Mexico full time, been down here almost a decade now, and I was just intrigued to find out, you look around and see so many expats and there were so many US citizens and other nationalities that were living here as expats, but there was no structured way to leverage to buy a home. And at that point in time, we were hoping that we'd be able to find those people who had come in and paid cash and were interested in harnessing that equity

Jose asks, "Is financing available only in tourist areas in Mexico?" That's a great question also. A lot of people think that we're only interested in the fancy beach destinations, and I like Cabo, that's the area that I live in. But there are many, many beautiful places around Mexico that people love to be in. So, the answer is no, MoXi services all parts of Mexico as long as we can legally close the transaction and the property meets the guidelines, meets our standards, then we're interested in talking with you. It's not just the tourist zones and the beach destinations. So, we were over in San Miguel de Allende just a few weeks ago. We've got a location that we opened up over there. Super excited about that. We see customers reaching out to us for areas like Mexico City, Guadalajara, the Lake Chapala area all over Mexico. And it's not just the sunny beach destinations, it's all over. Mexico is a beautiful country and we're interested in playing a part of you guys exploring all parts of it.

Kris says, "I've got a place in Tulum, the market's upside down. Should I sell, pull money out? What are the pros and cons?" Well, Kris, that's a tough spot. If the market is costing you money and it's not recovering, I'm sorry if the property itself is costing you money and if the market's not recovering quickly, maybe. And then you've got equity. If you've got equity in the value, maybe a cash-out refinance could give you the liquidity to stabilize your operations for a while, but you'd be adding to the debt, you'd be adding debt to that asset that may already be underwater. So, if that's the case, then maybe selling makes more sense for you.

If you could wait for a better market window and just ride it out, it might be the best option to sell it. Every scenario is different. We have a lot of people that talk about the Tulum areas and every market's got its ebbs and it flows. And what I'd recommend is to reach out to a mortgage advisor, take this conversation offline, let's get some hard numbers and some real world specifics on what it is that you're working with, and our team will be more than happy to guide you in the right direction. And if we can help you out and liquidate you a little bit, then that's a wonderful thing. But if we can just give you some guidance, then we'd be happy to do that as well. So, sorry to hear there's hard times over there. We know that's a tough spot. We definitely wish you the best and hope to explore this opportunity with you further.

Miguel says, "I own a house in Mexico, I want to sell it, buy another property in Mexico, or maybe use that money for a down payment on a house in the US." Well, we can help you Miguel on the, if you decide to buy a new property, we can help you there with financing on that new property or if you want to keep the property in Mexico and then refinance it and pull equity out, we could talk to you about doing that one. But we don't directly handle the sale or cross-border funds transfer. We wouldn't be part of the sale process of the property you have there. You'd want to work with your real estate agent, a closing team to manage how to navigate the sale and getting you paid on that property. Once you sell the home and those funds are available to you.

If your plan is to buy another home in Mexico, then we'd love to talk to you about using that equity that you got from the sale of that home as a down payment on a new place. And we'd love to talk to you about possibly doing the mortgage on your new home in Mexico. We do not loan on real estate in the United States at all. MoXi is a Mexican financial institution and our long-term fixed rate product is specifically used for Mexico. So, we can't help with the property in the US. But again, if you're looking to sell this one and buy another one in Mexico, please reach out. We'd love to participate in that with you. All right. Okay, so we're moving on through. I'm trying to watch the time as well. It looks like we're doing pretty good. So, let me see if I can get through these last few questions and then field a few live ones, pardon me, from today.

"Will MoXi finance to build $125,000 costs, with a $125,000 cost?" So, I wanted to cover this question even though we'd kind of already talked about construction financing in that, but I wanted to cover the loan size in this as well. So, MoXi doesn't finance construction. Again, we don't have a construction loan product where we can stage fund, but when the process is complete then and titled and everything's registered, then we could refinance it if the property is valued at more than $350,000. If that were the scenario, while $125,000 falls below our minimum threshold for a loan amount on our core product, then we could possibly look at doing an Anywhere loan for you. And that's another product that we have and we'll touch base on that one.

And the Anywhere program offers lending from 75,000 US dollars to 200,000 US dollars and it's a different type of loan. So, we'll touch base on that here in just a moment. Okay, I see some conversations going on in the chat, I'm wanting to engage over there, but I'm going to stay disciplined and move through our deal here. Okay, so this is a very good question. Gavin asks, "We own property through a Mexican holding company and we run a business in Cozumel. Can our operating company be the borrower?" The answer to that question, unfortunately, Gavin, is no. MoXi only lends to individuals, the US citizens or permanent residents. We don't lend to corporate entities specifically. Even if you own a hundred percent of the company, you'd have to take the loan out with us personally with the property held in a fideicomiso trust in your name. So, there's a little bit more to unpack here. So, let's kind of touch base on that real quick.

First of all, if you own the property and you own it through a Mexican holding company, then you hold title most likely through an escatura, not a fideicomiso. Fideicomiso is specifically designed for foreigners to own real estate in Mexico, but if you have the Mexican entity, then you would hold title in an escatura. That type of title would disqualify from MoXi's program because we do require for reasons that include what's been approved and registered with our investor, also what's been approved, registered with the Mexican government for our business practices and whatnot, we do require that any loan that we close be held, that title be held in a fideicomiso, even if it's not in the protected zones. It's a little bit different structure, but it's still a fideicomiso that you're going to get throughout all of Mexico. So, if the property's held in escatura, meaning that your Mexican corporation holds that title, then we wouldn't be able to do that. There's another piece here that kind of excluding the Mexican holding company.

Let's say for example the home was held in a US entity, we do allow vesting in entities for whatever reason may make sense to you as the borrower. So, we do have some customers who will establish a US entity. They will obviously apply individually, so the individual members of that entity must be on the loan and they all qualify personally and they're personally responsible through signing a personal guarantee and again, individual qualification. But MoXi will allow properties to be held in a foreign entity for tax purposes from a vesting perspective, but not to a Mexican corporation specifically because of the type of vesting on title. And again, it would be the individual that would have to guarantee the loan, not the company. Kind of got in the weeds there a little bit. I hope I answered that without adding confusion to the topic, but hopefully that answers your question there. Please feel free to reach out if I can expand or clarify.

Rita says, "How can I buy in Mexico if I'm a US citizen? Will I own the land and which restrictions are there?" Back to the fideicomiso and the type of title. In Mexico you can. So, here's kind of the rundown more especially for protected zones, but again, we apply the fideicomiso restriction all across the country. The Mexican constitution basically carved out specific pieces of real estate. I always get this backwards, but it's either 50 kilometers from the border and a hundred kilometers from the coast or vice versa. I think I've got that backwards. I think it's a hundred from the border and 50 from a coastline. Those areas are classified as what's called protected zones, if you will. And the Constitution states that in order to own fee simple, fee simple in our previous question would be an escatura, right, not a trust, which is a fideicomiso is a real estate trust.

In order to own real estate notice protected zones, fee simple or in the traditional sense you have to be a Mexican citizen or a Mexican entity such as the Mexican holding company that we answered the question about a moment ago. But foreign investment also written into the Mexican constitution as a provision to where we can get a permit from the Secretary of Foreign Affairs and we can establish a real estate trust or a fideicomiso as the title document to where a foreigner can actually hold and own real estate in Mexico. The difference, obviously there's trust structure and there's several different elements that are great selling points to doing it that way, but ...

What you do, where I lost myself a moment ago, is that setting up the fideicomiso, you essentially set up a bank trust, you name a Mexican financial institution as your trustee or your fiduciary, and then you just pay an annual renewal fee for your trust. It's a 50-year renewable trust and you pay an annual, I guess a maintenance fee that we collect for you monthly in your payments and keep taking care of there. But absolutely you can buy by using the fideicomiso. Please reach out to one of our mortgage advisors to get more details on that.

"My question is about capital gains tax in Mexico. How are they derived and how to avoid them?" Ron, we're going to have to recommend that you talk to a Mexican attorney or a CPA. We don't want to give you advice on that perspective, but I can tell you that capital gains tax in Mexico can be very complex, especially for foreigners. The rate and the exemptions depend on how long you've owned the property, how you've used it, occupancy, similar to things in the United States, how you've documented any capital improvements you put into the property. For example, if you bought this home and remodeled it, did you save your receipts and not just save your receipts?

Did you have facturas or proper receipts for those? Did you record that with the government? Things along those lines. It gets pretty deep. So, I always recommend working with a cross-border tax advisor and somebody who understands both US and Mexican tax law. I can't tell you that we will provide the documentation from lender perspective that could support you there. And we also from a servicing perspective, provide the documentation for the interest that you pay into the loan. But from a capital gains perspective, we're going to absolutely recommend that you take a hard look at that with a professional like an attorney or tax professional that can serve in those areas.

Jose asks, "How does it work? Do we apply through banks?" No sir. You'll apply directly with MoXi on our website or through one of our professional mortgage advisors. Again, we have an application right there on our website if you want to go to there, or if you're talking with one of your mortgage advisors, they can provide you with a direct link so that it'll come right into their queue and they can get you started. We are not a bank, we're a mortgage lender backed by US Institutional capital. The funding comes from investors who specialize in cross-border lending, which is why we can offer fixed rate fully amortized loans. Okay. All right, so the next question is from David. David says, and David, we get this one a lot also.

He says, "How competitive are the interest rates?" So, let me see if I can cover that real quick. So, our interest rates are very, very competitive within the cross-border financing space, and there's reasons for that. One is that we're fully fixed, fully amortized, we loan in service in US dollars. Most options, the very few options that there are for foreigners to finance rely on variable rate loans, peso loans, short-term structures, just very complicated way of doing things. I believe that MoXi is now one of the only, if not the only lender left doing full long-term, fully amortizing, fixed rate mortgages. Many have come, many have tried. We know this is a tough space. We are in it and learning and navigating our way through it, but we are proud to say that MoXi's got this thing down and we offer long-term fixed rate mortgages.

Let me get real. On our website we've got a page. It's our pricing page. So, you can either select the dropdown and look at rates and pricing, or you can just navigate to www.globalmortgage.mx/pricing. Okay. And this page gives you a nice visual of what I'm about to talk to you about. Okay, so interest rates with MoXi are calculated very similar to the way they are ... Thank you so much, Guillermo. Calculated very similarly to the way that they are in the United States, and there's a couple of different components. So, I'm going to try to stay out of the weeds with this question, but I'm going to try to explain it to you clearly. Okay. So, for a mortgage loan, whether it's a fixed rate mortgage or an adjustable rate mortgage, or even an interest only mortgage, whatever the type is for a mortgage loan to arrive at an interest rate, you've got to consider a couple of different components.

The first component that you'll consider is the index or some sort of a fiscal benchmark is our basis for your pricing. With MoXi you'll see on our pricing page that we're tied to the three-year treasury bond. That moves throughout the day, all day, every day, sometimes overnight and overnight trading. This is moving around all the time. So, this is what is fluctuating based on market conditions and things along those lines. Okay, so you have your index and that's again going to be the fiscal instrument or financial instrument your loan is tied to. Then you have another component that's called the margin. The margin is basically the investor spread. This is what the investor charges based on the risk-based criteria that the borrower brings. Your margin is going to depend on your credit score, your loan amount, and your loan to value.

So, it's going to depend on what your credit history is and how high your credit score is. Of course, a 780 is going to have a lower margin than a 720, let's say. It is also going to determine your loan to value. So, again, the bigger the down payment, the lower the margin type thing. So, we have now the index of the three-year treasury. We have the margin, which is based on the risk-based criteria. Again, credit score, loan amount, loan to value. You add the index plus the margin, and that gives you your interest rate. So, an example would be today, let's say we have an index of 3.5 percent. Let's say that the three-year treasury is trading at 3.5 percent. We're getting ready to close your loan, it's time to lock. Then we're going to see that index at 3.5 percent. It's the intraday high of the day that we lock the loan.

But for example, let's call it a flat 3.5. And then let's say that you have a margin based on credit score, loan amount, loan to value, and let's say that is 5.5 percent as an example, and that's going to be based on credit score, loan amount and loan to value. We would add those two together and that would be an interest rate for this example of what is this 9%, right? So, with that said, that's how you arrive at the interest rate. To break it down into easy-to-understand and what we can guide ourselves by from the day-to-day as we're watching the markets move. Most of the time you're going to find MoXi rates to be approximately two to two point a half percent higher than your 30-year fixed rate mortgages in the United States. So, again, if you're watching the news and you're seeing that interest rates are at 7.5%, or let's just say 7% in the United States, well then you could expect MoXi rates for a similar loan to be somewhere in the nine to nine and a half range.

So, for rough figures, just brainstorming, thinking about what you're getting ready to do, we're going to be on average about two to 2.5% higher than what you'd see on your traditional 30-year fixed. But every situation's different. We've got a very formulaic way of approaching those interest rates. So, your mortgage advisor could give you more specific and targeted examples of what that would look like for you. So, hopefully that gives you, again, dove into the weeds there a little bit, but wanted to expand on how MoXi calculates interest rates. We do lock just before closing, your mortgage advisor could tell you a little bit more about that. But again, interest rates are arrived by adding the index to the margin that ends up being your actual interest rate. And then once you close the loan, your rate is fixed for the duration. So, it's the same interest rate until you pay the loan off.

Mary. Let's talk about seller concessions. That's a great question and I'm glad you asked that because this is one that I think would really improve or really bring us a lot closer to what we're accustomed to in the United States. Okay, first of all, let me first say that mortgage financing in Mexico is a relatively new phenomenon.

We've been here since 2017. When we started out, there was nothing else out there. We've worked hard over the last few years to learn and improve in the process, but even still today, a lot of real estate agents and a lot of people don't even realize that there's financing available and some real estate communities are reluctant to have these conversations because it's just unfamiliar. One of the biggest things that we offer in our guidelines, one of the biggest benefits is that since we're structured very similarly to guidelines in the United States, we have a provision that allows for a seller to contribute towards a buyer's closing cost. Closing costs in Mexico are quite a bit more expensive than they are in the United States. I'm surprised we didn't have more cost specific questions this go-around, but they are quite a bit more expensive here in Mexico than they are in the United States.

And in the United States it is very common. Almost every real estate transaction has some sort of concession negotiated into the transaction to where the seller contributes part of their proceeds to support the buyer and some of their costs, we call that seller paid closing costs. So, MoXi has a provision in its underwriting guidelines in our credit policy, and it basically says that we will allow a seller to pay up to 6% of the purchase price of the house to be applied towards buyer settlement charges. So, that could be a direct credit to the buyer to reduce their necessary cash to close to be applied towards paying down some of their closing costs.

So, MoXi does allow for that. The way you would approach that when working with your real estate professional is they would make the offer, they'd structure up the purchase sales price, maybe in lieu of a direct discount, which may be emotional for the seller or worrisome for people working in certain markets driving down values and whatnot. But maybe instead of negotiating a direct discount, maybe they say, rather than doing a discount, you can make a concession towards your buyers or towards the buyer's closing cost. So, in essence, it nets out to be a discount to the buyer, but since it's a credit to closing costs, it helps them to reduce their necessary cash to close. So, we do have that available.

What's the biggest misconception foreigners have about buying property in Mexico? Well, there's so many. So, a lot of people think it's a 99-year lease and there is such a thing as ejido property. That's a whole different conversation. That is not something that we do. A lot of people think that they cannot actually own real estate in Mexico as a foreigner. That's simply untrue. Through using the fideicomiso, you can absolutely hold title. So, there's quite a few. All right, yes sir. Let me find this one.

Did you know that MoXi funds & services loans in USD, is regulated and audited in the US & Mexico, and ensures compliance throughout the term of your loan?

Try our MoXi Mortgage Estimator