Mexico Mortgage Rates: What U.S. Buyers Actually Pay

You found the place. Maybe it's a condo in Puerto Vallarta with an ocean view that doesn't make sense for what they're asking. Maybe it's a colonial in San Miguel that costs less than a teardown in your hometown. You've done the math, you've walked the property, and now you're asking the question that everyone asks:

Can I finance this? And what's it going to cost me?

The short answer: yes, U.S. citizens can get a mortgage in Mexico. But your options look different than what you're used to stateside, and Mexico mortgage rates vary widely depending on which path you take.

Let's get into it.

Financing Options for U.S. Buyers in Mexico

If you're a US citizen looking to finance property in Mexico, you have a few options. Each one comes with tradeoffs.

Pay cash. Simple. No interest, no lender, no monthly payment. But you're tying up a significant chunk of capital in a single foreign asset, and that money stops working for you the moment it leaves your brokerage account.

Peso-denominated mortgage from a Mexican bank. These average around 11.5% (or closer to 14% when you factor in all costs), according to Banco de México data. And that's just the rate. You're also taking on currency risk. If the peso moves against you, your effective cost goes up. If you're earning in dollars and paying in pesos, you're converting every month. That gets old fast.

Tap your US equity. A lot of buyers pull a HELOC or cash-out refinance on their primary residence to fund the Mexico purchase. The rate is often lower, sometimes significantly. A cash-out refi might land in the high 6s or low 7s. A HELOC might be 8% to 9%, though it's variable and can move. The process is familiar, the lender is domestic, and there's no cross-border paperwork. But there's a tradeoff: you're securing your Mexico purchase with your US home. If something goes sideways with the foreign asset, your primary residence is still on the hook. You're also pulling equity from a home you could sell in a few weeks if you needed to, and putting it into a property where sales can take months and the buyer pool is smaller. That's not necessarily wrong, but it's worth understanding.

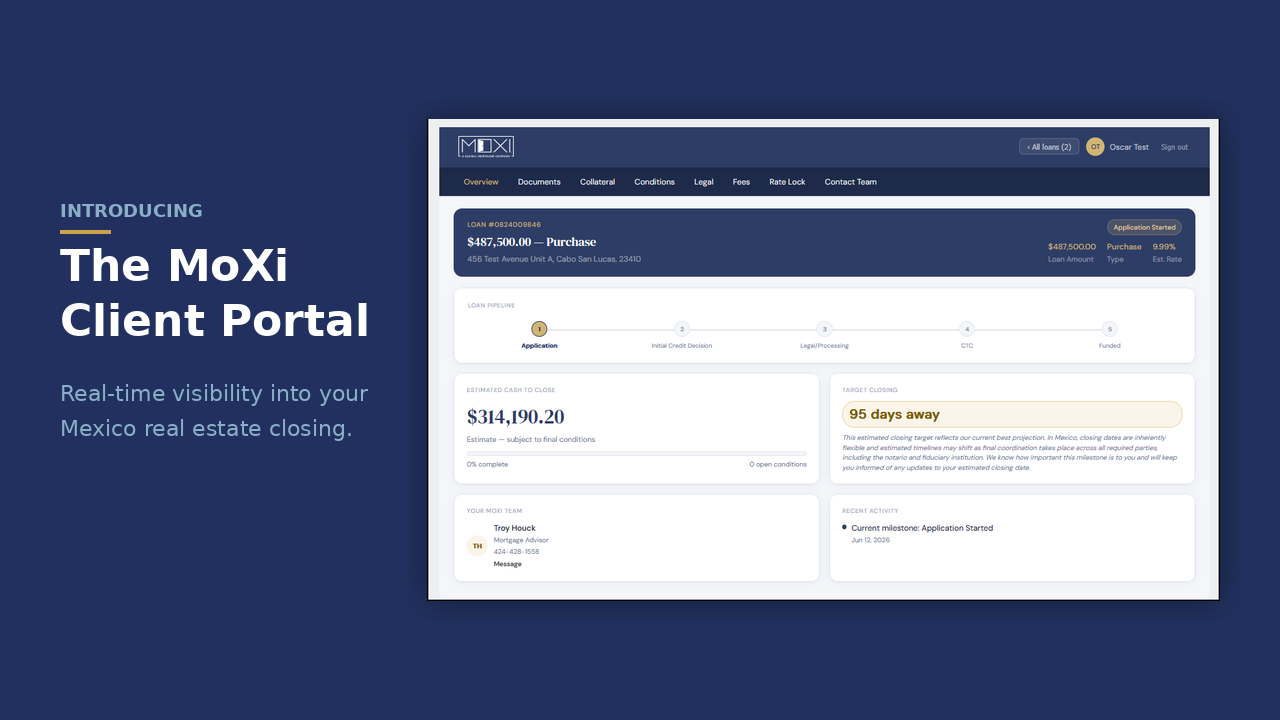

Cross-border USD mortgage. This is a narrow field. MoXi® is one of the only lenders offering USD-denominated mortgages to US citizens buying residential property in Mexico. We've been at this since 2017 and have closed over $150 million in cross-border loans. Rates typically land in the high 8s to low 10s for qualified borrowers. No currency risk. Fixed for up to 30 years. The debt is secured by the Mexico property itself, not your US home, so the risk stays isolated.

For comparison, a conventional 30-year fixed in the US runs around 6% to 6.25% right now. So yes, any Mexico financing option carries a premium over what you'd pay domestically.

Quick Snapshot

| Option | Rate Range |

|---|---|

| US 30-year fixed | ~6% to 6.25% |

| Mexican peso mortgage | ~11.5%+ (14% all-in) |

| HELOC on US home | 8% to 9% (variable) |

| Cross-border USD mortgage | High 8s to low 10s (fixed) |

The question is: why?

Why Cross-Border Lending Costs More

Here's the honest answer: cross-border lending is more expensive than domestic lending, and some of that cost shows up in the rate. Mexico mortgage rates are higher than U.S. rates for structural reasons, not because anyone's gouging you.

In the US, when a bank originates a mortgage, they typically sell it to Fannie Mae or Freddie Mac within weeks. Those agencies bundle loans into securities and sell them to investors worldwide. This creates a massive secondary market with constant demand, which drives rates down. The whole system is essentially subsidized by the federal government.

None of that exists for Mexico loans. When a lender funds a cross-border mortgage, that capital stays deployed. They can't package it up and sell it off. The cost of funds is higher, and that gets reflected in what you pay.

There's also the collateral question. Your property sits in Mexico, held in a fideicomiso (the bank trust structure that allows foreigners to own in the restricted zone). If something goes wrong and the lender needs to foreclose, that process runs through Mexican courts, Mexican notarios, and Mexican timelines. It's slower and less predictable than a US foreclosure. Lenders price that uncertainty into the deal.

And then there's just scale. The US mortgage market does millions of loans a year. Cross-border Mexico lending is measured in hundreds. Every loan requires hands-on coordination across two countries, two legal systems, and two languages. The fixed costs per loan are simply higher.

None of this is anyone's fault. It's just the reality of what it takes to make cross-border financing work.

It Works the Same Way in Reverse

Here's something worth considering: what does a Mexican citizen pay to finance investment property in the United States?

The answer might surprise you. Foreign nationals buying US real estate typically pay 8% to 11% on investment property loans, according to current market data. They're also looking at 30% or more down, 12 months of reserves, and zero access to Fannie Mae or Freddie Mac. The lender keeps these loans on their own books and prices them for risk.

Sound familiar?

Cross-border lending carries a premium in both directions. A non-US citizen buying in Phoenix faces the same structural realities you face buying in Puerto Vallarta: no Fannie or Freddie, credit verification across borders, collateral in a foreign jurisdiction, and higher per-loan costs for a niche product.

The premium isn't a Mexico thing. It's a cross-border thing.

How MoXi® Mexico Mortgage Rates Work

Our loans are up to 30-year fixed, fully amortizing, with no balloon payments and no prepayment penalties.

Your interest rate is calculated using a simple formula:

Your margin + the 3-year US Treasury yield = your fixed rate

The 3-year Treasury is public. You can look it up right now. As I write this, it's sitting at about 3.47%.

Your margin depends on three things: your credit score, your loan-to-value ratio, and your loan size. Stronger credit, more equity, and larger loans all get you a better margin.

For most qualified borrowers (think 760+ FICO at 65% LTV), that math lands you somewhere in the high 8s to low 10s, all-in. Your actual rate depends on your profile and where the Treasury sits when we finalize your loan, but that's the neighborhood.

When Your Rate Gets Locked

Once you have a property under contract with a closing date within 120 days, we'll issue your Initial Credit Decision and lock your margin. That margin is good for 120 days. The Treasury side of the equation will still float with the market, but you'll know your margin and can watch the index to get a sense of where you're headed.

One thing to keep in mind: you'll need to meet the same qualifying criteria at closing that you did at approval. Your financial picture needs to look the same. So if you're eyeing a new UTV or boat for the beach house, maybe wait until after you close.

About 48 to 96 hours before your closing, we finalize your rate by adding your margin to the intra-day high of the 3-year Treasury. That's your number. We draw up your loan documents, you close, and that rate is fixed for the term of your loan.

If you're still shopping for a property and don't have a contract yet, your margin floats until you go under contract. If you're buying new construction with a completion date beyond 120 days, same deal. Once you're inside that 120-day window, we lock it down.

Full details on our process are on the MoXi® pricing page.

Is It Better to Pay Cash or Finance Property in Mexico?

This is the real question, and the answer depends on your situation.

Let's say you're financing $400,000 at 9.5%. Your annual interest cost is around $38,000 in the early years. That's real money.

But here's the other side: if you pay cash, that $400,000 isn't earning anything. If it would otherwise be invested and returning 7% or 8%, your opportunity cost is $28,000 to $32,000 a year.

So the true cost of financing isn't 9.5%. It's the spread between what you're paying and what you'd otherwise be earning. For a lot of people, that spread is much smaller than it looks at first glance.

There's also the question of flexibility. Maybe you don't want $400,000 locked up in a single foreign asset. Maybe you'd rather keep that capital working and have some cash on hand for opportunities or emergencies.

This is where the "tap your US equity" option gets complicated. Yes, the rate might be lower on a HELOC or cash-out refi. But you're pulling equity from your US home, which you could sell quickly if you had to, and putting it into Mexico real estate, which moves slower. If you need to exit the Mexico property quickly, that market doesn't always cooperate. You can't always sell on your timeline. Meanwhile, your US home is carrying debt that funded an asset you can't easily unwind. With a cross-border mortgage, the debt is secured by the Mexico property. If you need to sell, you sell. Your primary residence stays clean.

On the other hand, if your money is sitting in a savings account earning 4% and you hate the idea of paying interest, cash might be the right call.

There's no universal answer. But framing it as "what would this money be doing otherwise" rather than "9% sounds high" usually leads to a clearer decision.

If You Want to Explore Further

We're a regulated financial institution in Mexico and operate to US standards. We built this thing because financing shouldn't be the reason someone doesn't buy a place they love. The process should feel familiar. The pricing should be transparent. And someone should be able to explain, in plain language, exactly what you're getting into.

If you're serious about buying, schedule a MoXi® Discovery Session to understand what your margin would likely be based on your profile. Or use our Mexico Mortgage Estimator to see what the numbers might look like for your situation.

Either way, you've got options. That's the whole point.

Frequently Asked Questions About Mexico Mortgage Rates

What are current mortgage rates in Mexico for U.S. citizens?

It depends on how you finance. Peso-denominated mortgages from Mexican banks average 11% to 14% effective. USD cross-border mortgages typically range from the high 8s to low 10s for qualified borrowers. HELOCs on U.S. property run 8% to 9% but are variable and secure your stateside home.

Can U.S. citizens get a 30-year fixed mortgage in Mexico?

Traditional Mexican banks rarely offer long-term USD loans to foreigners. Specialized cross-border lenders like MoXi® offer up to 30-year fixed USD mortgages secured by the Mexico property itself.

Is it cheaper to use a HELOC instead of a Mexico mortgage?

Often yes, on pure rate. But a HELOC secures your U.S. home, meaning your primary residence is on the hook for a foreign asset. A cross-border mortgage isolates the debt to the Mexico property, keeping your U.S. equity clean.

Did you know that MoXi funds & services loans in USD, is regulated and audited in the US & Mexico, and ensures compliance throughout the term of your loan?

Try our MoXi Mortgage Estimator