Five Things People Get Wrong About Buying a Home in Mexico

A lot of smart buyers walk away from the right property because of things they believe that simply are not true. Here is what the numbers and the process actually show.

Every year, thousands of U.S. Citizens and permanent residents buy homes in Mexico. Beach houses in Los Cabos, condos in Puerto Vallarta, colonial homes in San Miguel de Allende. And every year, a surprising number of them make decisions based on old assumptions that were never quite right to begin with.

Some of these ideas have been floating around for so long that people repeat them without ever checking. They cost buyers money, delay good decisions, and in some cases talk people out of a purchase that would have worked beautifully for them. Here are five of the most common, and what is really going on with each one.

Myth One

"You have to pay all cash."

This is the big one, and it is the reason we exist. A large share of Americans who buy property in Mexico still pay entirely in cash, and most of them do it because they assume financing is not an option. It is.

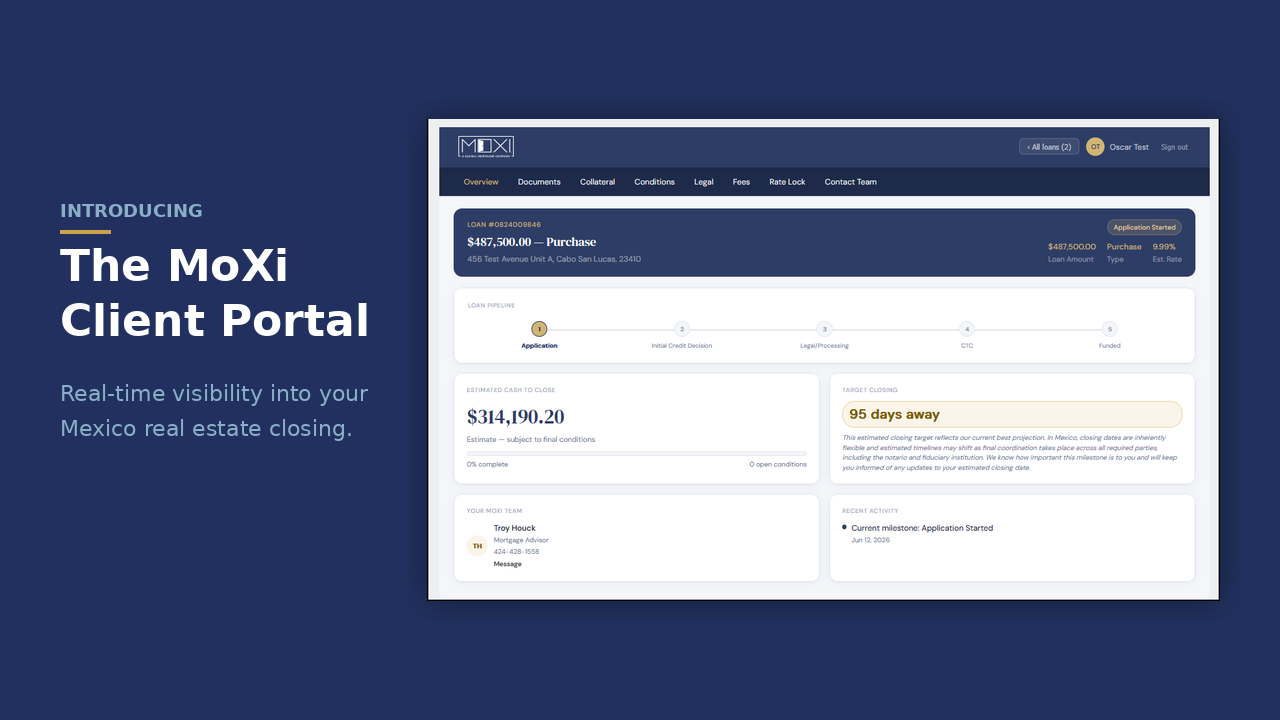

MoXi provides USD-denominated mortgages to U.S. citizens and permanent residents buying residential property in Mexico. Up to 30-year fixed, dollar-denominated, so there is no currency exchange risk on your payment. Loans run from $250,000 to $2.5 million. You do not need a Mexican credit history, because qualification is based on your profile in the United States.

Myth Two

"Americans cannot really own property in Mexico."

You can, and thousands of Americans and Canadians do it every year. The confusion comes from the "restricted zone," the strip of land within roughly 50 kilometers of the coast and 100 kilometers of a border. Inside that zone, foreign buyers hold property through a fideicomiso, a bank trust that gives you full rights to use, rent, sell, remodel, and pass the property to your heirs. Outside the restricted zone, in places like San Miguel de Allende, foreigners can hold direct title in their own name.

The fideicomiso is not a loophole or a workaround. It is the standard, government-established structure for foreign ownership near the coast, and it has protected buyers for decades. A MoXi-financed property uses a fideicomiso regardless of location.

Myth Three

"Financing in Mexico means a peso loan with a punishing rate."

If you borrow from a Mexican bank in pesos, rates have recently run well above 10 percent, and your payment moves with the peso. That is the picture most people have in their heads, and it is a fair reason to hesitate.

A cross-border USD mortgage is a different instrument entirely. You borrow in dollars, you pay in dollars, and your rate is fixed for the life of the loan. Your income is almost certainly in dollars, so there is no currency mismatch and no guessing what your payment will be next year. That is the whole point of a lender built for this specific buyer.

Myth Four

"All financing works basically the same way."

It does not, and this is worth understanding before you sign anything. When you buy a property in Mexico, you may be offered financing directly by a developer or a seller. That can be a genuinely good fit for some buyers, and there is nothing wrong with it. What matters is knowing how it is structured.

Developer and seller financing is often written as a shorter-term loan, sometimes three to five years, with a larger payment due at the end of the term. If you plan to sell or refinance before then, that structure can work fine. If you are planning to hold the home for the long run, a fully amortized 30-year fixed mortgage is a different tool, one where the loan is paid down steadily over time with no large payment waiting at the end.

Myth Five

"If I paid cash, my money is locked in the walls."

A lot of people bought their home in Mexico with cash, either because they had it or because they believed myth number one. Their equity is real, and it does not have to stay frozen in the property.

A cash-out refinance lets an owner borrow against the value of a home they already own outright, converting some of that equity back into usable dollars. People use it to fund a second property, reinvest, handle a major expense, or simply put idle capital back to work. If you paid cash for a home in Mexico, you have options that many owners do not realize are available to them.

The backdrop: values have kept climbing

One reason these myths cost people so much is that the market has not stood still while buyers hesitated. Across Mexico, residential prices rose in the high single digits over the past year, and the expat-favorite markets have moved right along with it.

In Los Cabos, home prices rose roughly seven to eight percent over the trailing year, with Pacific-side master-planned communities appreciating faster. Puerto Vallarta posted mid-single-digit gains overall, with view homes and the most walkable neighborhoods climbing eight percent or more. San Miguel de Allende ran even hotter, with the historic center appreciating at a double-digit pace. These are market figures reported by regional and national real estate sources, not projections from us, and they vary by neighborhood, property type, and timing.

The point is simple. Equity has been building for owners whether they financed or paid cash. And for buyers still sitting on the sidelines because of an assumption that was never true, the cost of waiting has been real.

Have questions about financing a home in Mexico?

A complimentary discovery session with a MoXi mortgage advisor walks you through how it works, what it takes to get pre-approved, and whether it fits your plans. No pressure, no obligation.

Book a discovery sessionMoXi® is A Global Homeownership Company. Loan products are available to qualifying U.S. citizens and permanent residents for residential property in Mexico. Loan amounts from $250,000 to $2.5 million, 30-year fixed, USD-denominated. Terms, qualification requirements, and availability are subject to review. Market appreciation figures cited are drawn from third-party regional and national real estate market reports and are provided for general information only. This article is educational and is not investment, tax, or legal advice.

Did you know that MoXi funds & services loans in USD, is regulated and audited in the US & Mexico, and ensures compliance throughout the term of your loan?

Try our MoXi Mortgage Estimator